One of the biggest challenges many prospective investors face is fi nancing. In recent years, home loans have been difficult to secure, with banks and major lenders implementing stricter criteria, even for buyers with excellent credit histories. This has made building a portfolio more difficult than ever and has complicated the entry of new investors into the property market.

Here is where affordability comes into play. With lowpriced properties, prospective buyers can apply for smaller loans, and this often increases their chances of being approved, since the servicing is lower – not to mention that the risk is lower for the lender.

“Due to their lower price range, budget properties require a smaller deposit and have a lower mortgage repayment,” says Peter Koulizos, coordinator of property and share investment in the Property Services department at TAFE SA.

“Your council and water rates, land tax and other levies should be proportionally cheaper as your land property is cheaper. And generally speaking, budget properties have a higher rental yield than more expensive properties in prime locations.”

Affordable dwellings can be found all over the country, in both metropolitan and regional areas, and indeed houses in Tasmania can generate rental returns of up to 7%, as an example. Affordable homes can come with considerable capital growth potential as well – some budget suburbs record double-digit increases in price.

In addition, budget properties can serve as good building blocks for a portfolio, as they help you diversify your risk of having your properties sitting vacant.

“I’d prefer to have ten $500,000 properties rather than one $5m property. If you own 10 properties and one is vacant, then 10% of your portfolio would be vacant,” explains Helen CollierKogtevs, managing director at Real Wealth Australia.

“However, if you have one property and it’s vacant, then 100% of your property is vacant. Plus, more people can afford to rent properties that have a price tag of less than $500,000.”

As advantageous as it is to buy affordable properties, buyers should be mindful that it’s not a foolproof solution.

Here are some of the risks involved in purchasing budget properties:

1. Budget properties may be in a poor location

1. Budget properties may be in a poor location

Not all affordable suburbs are in poor locations; however, from an investment perspective, they’re not always located in areas that are overfl owing with growth drivers. This could mean your portfolio winds up underperforming on rents and/or sale prices.

“It’s important to research any area under consideration to make sure the fundamentals support your investment, and that there are strong prospects for the area for future growth,” says Collier-Kogtevs.

The signs of a property’s potential for profi t or capital gain include population growth, infrastructure projects and the presence of a considerable rental population in the area.

“Purchasing a $500,000 property across the road from a train station may seem convenient; however, it may not be desirable to tenants, or buyers when it comes to selling,” Collier-Kogtevs explains.

It’s better to look for homes within walking distance of the train but without the roaring noise in their backyard.

2. Budget properties can attract problematic tenants

With affordable dwellings, you can afford to charge lower rents, which can attract many tenants. However, if you buy in a low socio-economic area, you could be inviting a lot of trouble.

“The tenants that target these types of properties may give you more grief than tenants in more expensive properties which are located in prime locations,” says Koulizos.

Properties in such areas are likely to be more rundown as well, which could turn off the kinds of tenants you want. You also want to look into the crime rates and demographic in the suburb, along with the condition of the property, before you commit. A good property manager can help you avoid the trouble of a problematic tenant and handle any issues that arise.

However, if you are managing your investments personally, you need to be extra careful.

“Formulate a watertight tenant selection process, and conduct all the required due diligence,” Koulizos advises.

3. Budget properties don’t necessarily mean lower expenses

Buying an affordable dwelling may seem ideal for your wallet on the surface. But in the long run the wrong property could cost you more than you expected.

“Even though a property might be cheap, it doesn’t mean that all the rental expenses are proportionally cheap,” Koulizos points out.

For instance, things like heaters and tradie services cost the same regardless of a property’s value. A plumber will charge a $100 call-out fee regardless of whether the property is worth $200,000 or $800,000 – and if the home you purchase ends up requiring a lot of repairs and replacements, the money you think you’ve saved on a cheaper property will soon be chewed through by expenses instead.

.JPG)

While you can definitely add value to a property through renovation, you ultimately need to determine if the process will cost more than you will be able to gain if you sell or rent it out.

“If you do purchase properties that are cheap, old and in need of maintenance, then you will end up with additional costs that will impact your cash flow,” says Collier-Kogtevs.

All of these risks can be mitigated by being diligent with your research, inspecting prospective properties and getting the right tenants. You can also balance your portfolio by investing in some more expensive properties in more popular locations, in order to better guarantee growth.

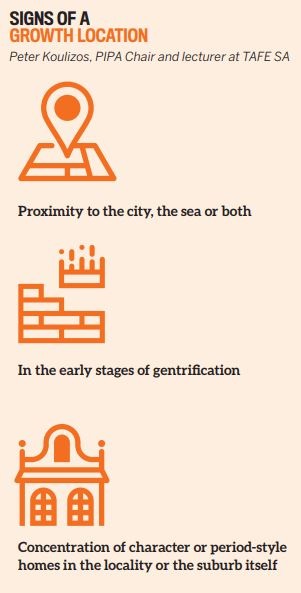

In addition, having your finger on the pulse of what’s up and coming in the area will not only help you know where to buy but also get you in on a blossoming market early. Properties with potential that could currently be undervalued include those that are close to the city and/or the shore, that have a collection of character or period homes in the area, and that are starting to gentrify.

“I always like to ask property managers about the areas or streets in the suburb a tenant would want to live in. The answers help to narrow down your search to a handful of streets, making it easy to select a good investment,” Collier-Kogtevs says.

“Follow the growth, where the people want to work and live, and where the infrastructure investment is happening. Remember, property investing is for the long term, so it’s important to have a long-game mindset.”