Investing in a rental property may give you positive cash flow and an asset that will grow in value. However, it may also come with potential threats.

As a landlord, you may be at risk of having poor tenants who could damage your property, makes late rent payments, or doesn’t treat the property with respect and gets complaints from neighbours.

Having landlord insurance may help you cover from losses connected with your rental properties. It is an insurance specifically written to protect against risks most landlords may face.

Although not a legal obligation, many property management teams now require landlords to have insurance coverage before taking on a new property. It’s now standard in the industry for property managers to discuss financial risks a new landlord may encounter and provide guidelines on how to handle these risks with a comprehensive landlords’ insurance policy, according to the Real Estate Institute of New South Wales.

Landlord insurance usually includes coverage for the following:

- Fire

- Theft

- Loss of rent

- Legal liability

- Vandalism

- Flood

- Emergency repairs

- Earthquake

Why you may need it

Landlord insurance offers protection for both landlords and property managers. It may minimise risks for everyone and may make your job as a landlord a bit easier. Some of the benefits you may have with a landlord insurance policy include:

- Rental loss coverage. Loss of rent comprises more than half of landlord insurance claims, according to Carolyn Parrella, executive manager of Terri Scheer Insurance. With landlord insurance, you may be able to claim loss from your property being damaged.

Coverage for rental loss may only apply when a property is inhabitable. You may also have to collect evidence proving that your rental is damaged and needs coverage.

- Property damage coverage. Some landlord policies may cover payment for property damages. They may cover damages that buildings and contents may have due to natural disasters. Some policies may also cover malicious damages that tenants may make, such as vandalism.

- Liability protection. Landlord insurance may protect you and your rental property from injuries or death that may occur on your property.

For example, if a tenant gets seriously injured, they may sue you—the landlord—for damages. Your landlord insurance may cover you from this.

- Emergency coverage. Some landlord insurance policies may provide emergency coverage. You may be able to claim for incidences like leaks or a tenant being accidentally locked-out.

An emergency coverage may also include costs incurred to travel to and from the property to resolve an issue.

- Legal costs coverage. No one wants to incur thousands and thousands of legal costs. Landlord insurance may cover for legal expenses you may incur when resolving legal issues with a tenant.

Home insurance is NOT landlord insurance

Many investors may think that their home insurance is enough to cover their rental properties. However, this isn’t always the case. Home insurance generally will not protect you from rental loss and malicious damages done by tenants – coverage that landlord insurance provides.

Here are damages or losses that BOTH home and landlord insurances may cover:

- Fire

- Storm

- Flood

- Impact

- Legal liability

- Water damage

However, ONLY landlord insurance may provide coverage for the following damage or loss:

- Rental income loss

- Legal expenses related to eviction

- Malicious damage

- Accidental damage

You may not need an additional home insurance policy if you already have a building and contents insurance as part of your landlord insurance. However, if you only have tenant protection, which doesn’t cover you from building damages or theft, you may need additional building insurance or content insurance.

Average costs

Landlord insurance can cost as little as a few hundreds of dollars per week. However, this cost depends on the state where your rental property is located. Some considerations that may go into calculating the cost of your landlord insurance include risks associated with your property, local crime statistics, and natural disasters prone to your rental property’s location.

Optional benefits covering vandalism, tenant theft, fixtures and fittings may also affect the cost of your landlord insurance.

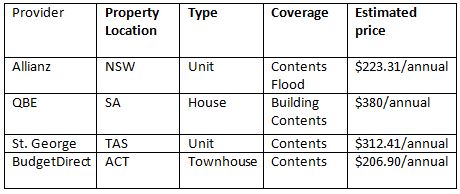

Here are sample costs of landlord insurance based on various providers, as of December 2019:

These calculations were made using the landlord insurance providers’ online calculators. To get an estimated quote that you may need to pay for your policy, talk to your preferred provider.

Some of landlord insurance providers in the country are:

Choosing the best landlord insurance

Landlord insurance may seem like just an additional cost to your existing rental maintenance and management expenses, but it’s a policy that may help you protect your investment from future issues. To choose the best policy for you, consider the following:

- Evaluate the coverage you may need. Consider your property, its value, and contents when deciding what features you want a landlord insurance policy to have. Do you need coverage for building only? Do you need coverage for both building and contents? The features or benefits you want for landlord insurance may affect how much you need to pay, so consider these carefully.

- Shop around. Compare landlord insurance from various providers by looking at the coverage and benefits they offer and their estimated costs. To do this, you may look use the providers’ landlord insurance calculators and get an estimate. You may create a checklist to compare various providers.

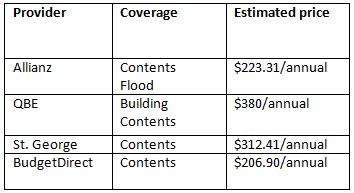

Sample comparison checklist:

- Consider your property’s location. Your rental property’s location also affects how much you must pay for landlord insurance. If your property is in an area prone to natural disaster, you may want to consider this when choosing a policy. It also means you may have to pay a bit higher for landlord insurance.

For example, you have a rental property in a flood-prone area such as Queensland; this will be considered when a provider computes the amount you must pay for a policy.

Landlord insurance may benefit you and your investment portfolio as it protects you for future issues related to your rental. It has become standard practice because of the risks of liability and damage to an investor’s rental which may result in financial loss.

Speak with an insurance agent about your options and discuss what’s best for you and your property.

Always double-check the fine print to make sure that your landlord insurance covers the basics and any additional provisions you desire. Some additional provisions for coverage that you may consider include building codes, burglary, rental property under construction, or damages caused by pets.