Capital cities in Australia are expected to witness record dwelling-price growth next year, but the two biggest markets could remain vulnerable, according to a new study by SQM Research.

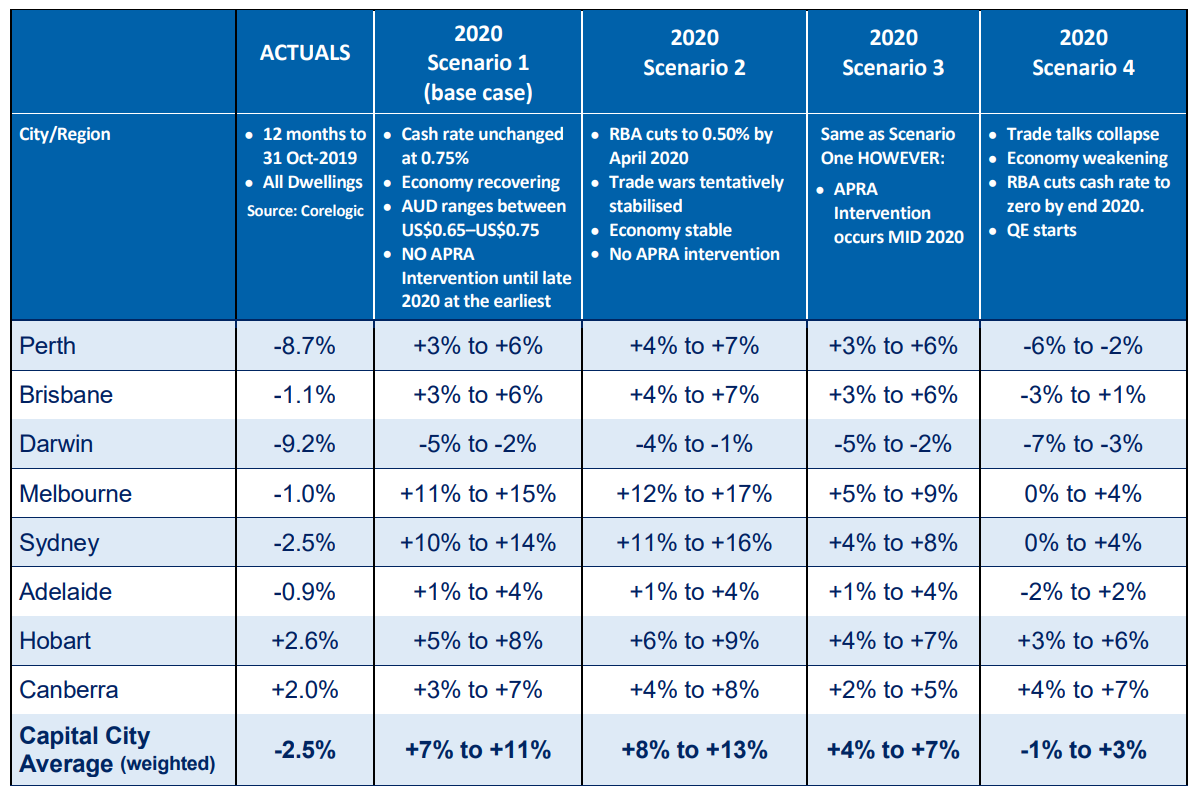

The company’s “Housing Boom and Bust Report” laid out four likely economic scenarios and their impacts on house prices. The base-case forecast is for dwelling prices to rise between 7% and 11%, driven by Sydney and Melbourne.

Best-case scenario

SQM Research's base-case forecast assumes no changes in the Reserve Bank of Australia’s (RBA) cash rates and no intervention from the Australian Prudential Regulation Authority. The scenario also takes into consideration a positive economic response from the three rate cuts this year and reduced trade tensions.

Also read: Property values down by 8.4% since 2017

Under this scenario, the forecast is for Sydney and Melbourne to witness growth of as much as 14% and 15%, respectively. Other capital cities are also expected to post record-high gains.

SQM Research managing director Louis Christopher said these capital cities, particularly Sydney and Melbourne, have benefitted from the three interest-rate cuts this year, as well as from the loosening of credit restrictions and the strong population growth.

"These factors are expected to drive the national housing market into 2020. In a close call, APRA is expected to not immediately intervene despite the strong price rises," he said.

Sydney, Melbourne not the best bet

Despite the strong price outlook for Sydney and Melbourne, these cities are likely to remain vulnerable, Christopher said.

"We have some misgivings on the sustainability of this new recovery. Sydney and Melbourne are rising from an overvalued point. Long term, our two largest housing markets look vulnerable and forever reliant on cheap credit," he said.

Christopher believes that better value can be found in other capital cities like Brisbane and Perth, which are both going to benefit from the recovery in mining investment.

What could make things worse?

The worst-case scenario under could see prices go between a fall of 1% and a gain of 3%. Under this scenario, the economy would not respond to the rate cuts, pushing the RBA to bring rates to 0% by the end of 2020. This scenario also assumes a quantitative easing.

Should this circumstance play out, Sydney and Melbourne prices could remain flat or grow by only 4%.

The table below shows the price forecast in each capital city under four unique scenarios: