Property investing can be an excellent way to create a passive income, especially in areas where supply is tight and demand is high.

However, it’s not an undertaking that comes without risk. As a landlord, one of the biggest risks you face is a dodgy tenant who doesn’t do the right thing by you or your property.

Terrible tenants are everywhere, and no landlord is ever exempt from the chance of getting one.

You could encounter one of those renters who forgets – or doesn’t want – to pay their rent on time, and you have to chase them up constantly each month for what they owe.

You could get a tenant who sneaks in pets against your wishes. Or you could hit the jackpot with renters who are party animals – not only do they make a racket that incites complaints from neighbours, but your property can be left an almighty mess when the smoke clears.

These are just some of the risky tenants out there in the rental pool, which is why it’s important to screen potential renters stringently and take steps towards enforcing strong risk protection policies for your property, for example by having comprehensive tenancy agreements and conducting regular inspections.

“The insurance policy allowed Jin and her property manager to claim for months of lost rent, and loss of rent when the property was untenantable”

Even then, the vetting process is not likely to be 100% bulletproof as a sketchy tenant is always able to put their best foot forward until they have actually moved in.

Nightmares can come true

Carolyn Parrella, executive manager at Terri Scheer Insurance, has seen plenty of bad tenancy cases in her time, including one incident that cost a client over $14k in damage and repair fees.

“This landlord, Jin, owns an investment property in Edmondson Park, Sydney. The house was brand new, with no previous tenants. Her first tenants were a young couple in their thirties and the weekly rent was $600,” Parella says. “The tenants frequently missed payments and tried hard to avoid being evicted when confronted for not paying.”

The loss of rental profit put the client under financial strain, because she still needed to pay the mortgage and the utility bills.

Terrible tenants are everywhere, and no landlord is ever exempt from the chance of getting one

Finally, the client’s property manager initiated the process for forced eviction through the civil and administrative tribunal in NSW.

After four months of deliberation, the tribunal granted the lease termination. However, the tenants did not go without a fight.

“When the tenants were evicted, the property manager found they had also deliberately and maliciously damaged parts of the property. Some items had also been stolen,” Parrella says.

All in all, the costs of eviction, damage, unpaid rent and repairs amounted to a whopping $14,435.36 in total.

Fortunately, the client had taken out comprehensive landlord insurance on the property, which served as financial protection as it covered the expenses, including damages (accidental, deliberate and malicious), theft, lock replacements and legal costs.

“The insurance policy also allowed Jin and her property manager to claim for months of lost rent, and loss of rent when the property was untenantable while repairs were completed, which took around four weeks,” Parrella says.

“It included claims for multiple insurable events, none of which could have been foreseen when her tenants entered the property.”

This highlights how crucial a solid insurance policy can be for an investor, even if you already have a good and trusted property manager. An effective property manager can definitely assist you in preventing many mishaps, as well as in addressing problems, but there is also only so much they can do, whereas insurance can enable you to recoup losses.

This highlights how crucial a solid insurance policy can be for an investor, even if you already have a good and trusted property manager. An effective property manager can definitely assist you in preventing many mishaps, as well as in addressing problems, but there is also only so much they can do, whereas insurance can enable you to recoup losses.

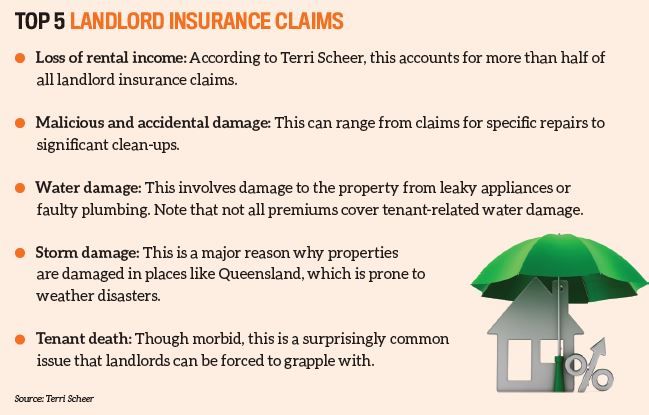

A standard landlord insurance policy can cover loss of rental income and damage to or theft of the contents of the home, although precisely what is covered can vary. Typical claims include losses due to rent arrears, water damage and malicious/accidental damage by a tenant.

Policies can also differ based on whether you’re managing your rental property personally or via a third party, and coverage can vary based on whether the home is being leased out as a short-term rental (such as through Airbnb) or a long-term tenancy.

Make it a point to determine what you need and find the best possible insurance provider that offers a premium to fit your requirements. Insurance premiums vary across states and territories – for instance, in a cycloneprone area like northern Queensland the fees are higher to cover storm damage.

Landlord insurance is a valuable lifeline for investors, but of course that shouldn’t mean landlords can afford to be lax about ensuring they don’t sign up bad tenants in the first place. These nightmares can often be circumvented by conducting thorough background checks on potential renters.

You (or your property manager) should aim to speak to not only the most recent landlord but previous ones as well, in order to determine any behavioural patterns that could prove problematic in the long run. It also helps to ensure that the prospective renter’s current landlord is not just trying to get a nightmare tenant off their hands. As much as possible, prod them to go into detail about what kind of tenant the person has been.

Bad tenants can make your life miserable for a time but don’t need to be allowed to destroy it. You can avoid this by having the right protective measures in place.