Since Australia was first impacted by COVID-19, a flurry of national economic commentary ensued. A series of fiscal and monetary interventions were deployed to mitigate the projected damage. Australia has fared quite well so far, but this came at a cost. According to data from the Australian Office of Financial Management, more than $122 billion of extra government debt was issued in the first half of the year, equivalent to about 6.4 percent of GDP. With no signs of slowing in the coming months, it is likely our swelling debt will continue, albeit at a lower rate than many other developed countries.

Despite negative forecasts made by some, the property market has fared well so far. Data from the Real Estate Institute of Victoria indicates that metropolitan Melbourne prices have had a mild downturn, returning to late-2019 prices. Regional Victoria, however, has seen positive dwelling price performance—validating predictions that post-pandemic Australia may reorient to the countryside. I see this as a temporary phenomenon, but that hasn’t stopped areas such as the Blue Mountains to Sydney’s west achieving record median sales prices.

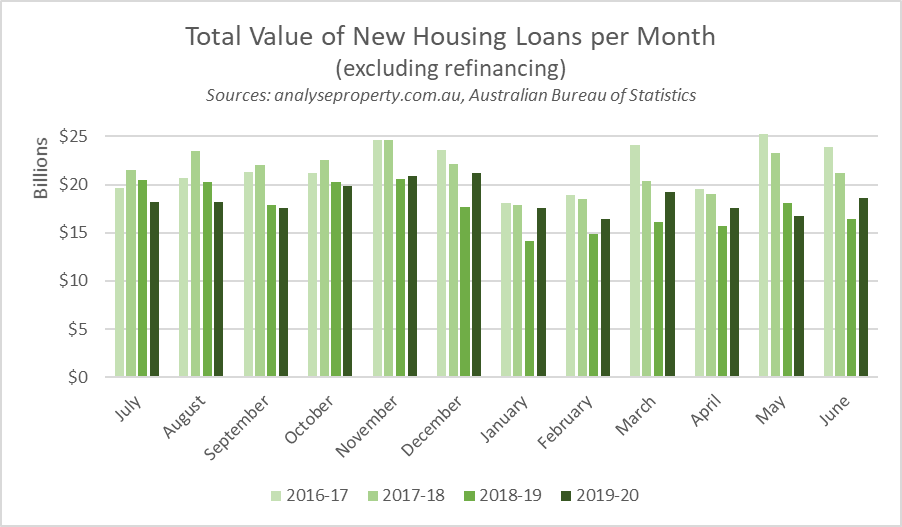

Undoubtedly fueling Australia’s curious property performance during the first half of the year is growth in housing finance. According to the Australian Bureau of Statistics, each month of 2020 (except May) experienced a higher volume of new housing loans than the corresponding month in 2019. This suggests that COVID hasn’t been as much of a deterrent as last year’s factors were, such as federal election uncertainty and lending growth constraints. As a result, the 2019-20 financial year also experienced growth in new housing finance, the first time since 2016-17. We have also seen the RBA cash rate fall by 125 basis points in the space of 12 months which strengthened mortgage serviceability for those securely employed.

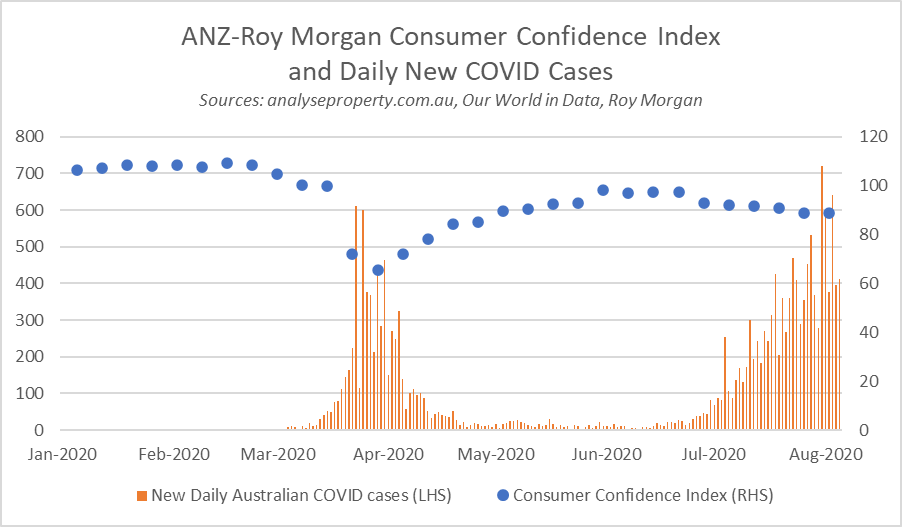

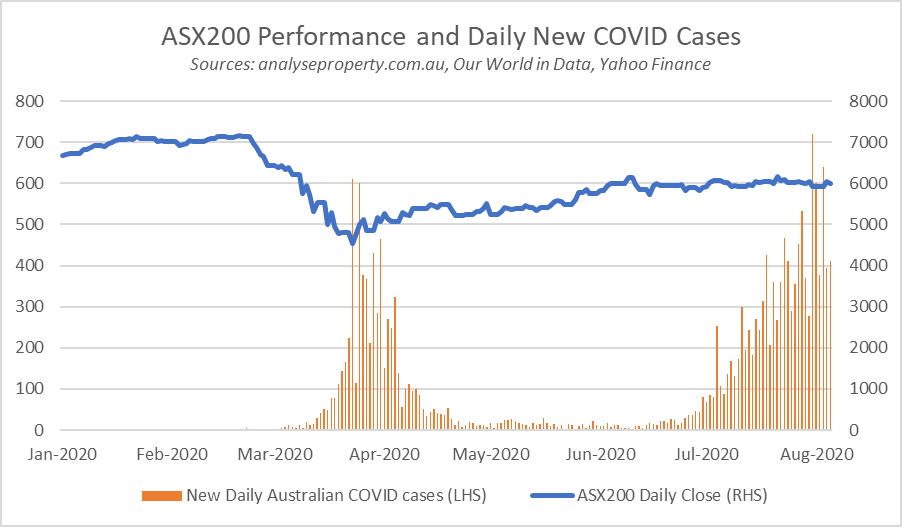

The multibillion-dollar question is whether recent resilience is sustainable, and whether Australia can navigate through the pandemic with little more than a government debt hangover. This depends on a multitude of factors, notably the necessity of each household making use of mortgage holidays, as well as the time it takes for a vaccine to eliminate the public health threat. Evidence of Australia’s strengthening resolve can be seen in data which suggests the second spike has had less of a sentimental impact than the first—even though the second is greater in severity than the first. We can observe this through two separate lenses which suggest the “new normal” we keep hearing about is upon us.

1) ANZ-Roy Morgan Consumer Confidence Index

When coronavirus cases first began to skyrocket in Australia, the ANZ-Roy Morgan Consumer Confidence Index plummeted from 100 to 72.2 in the space of a week. It progressively recovered week-on-week until signs of the second wave began to emerge, but the downturn in confidence has no resemblance to what was experienced during the first wave.

2) The Australian Securities Exchange

The market capitalisation of the Australian Securities Exchange is meant to reflect the value of listed companies, but it is often a more accurate indicator of sentiment. On 20 February, the ASX200 peaked at 7,162 and by 23 March it had bottomed out at 4,546—a fall of 37 percent in just a month. The market began its recovery the day after the first wave peaked, showing how responsive it is to perception. The same didn’t take place once the more severe second peak emerged, implying a form of short-term market immunity. This could contribute to explaining why Australians have been comfortable borrowing more money to buy homes during the pandemic.

Although uncertainty continues to make things difficult for short-term forecasts, it appears that Australian resolve has partly contributed to the comparatively strong outcomes we have experienced to date. If we are able to successfully defeat the virus and get everybody back to work without the assistance of too much government stimulus, some of us may even end up better off for the experience!

Luke J. Graham is an organisational behaviour and property market analyst. He is currently completing postgraduate studies at the University of Oxford.