Becoming a savvy investor isn’t something that happens overnight. While some people possess more aptitude than others, any successful investor will have benefited from years of experience, mentoring and access to the knowledge of others.

But that’s not to say there aren’t ways to effectively harness such knowledge and distil it into an accessible form. With more than 15 years of experience in property investment across multiple strategies ranging from capital growth and positive cash flow, through to small- and largescale property development, Simon Buckingham, director of Results Mentoring, has developed a variety of tools to aid new and existing investors alike.

“We train people to become well-educated and sophisticated real estate investors who sensibly use property as part of their investment portfolio,” says Buckingham.

He explains that there are five key steps that should guide any investor who is looking to expand their portfolio: creating your strategy, unlocking finance, finding the right property, negotiating amazing property deals, and establishing effective management.

“Whether you’re brand new to investing or have already built a portfolio, they’re valuable ways to look at your current situation and reassess your strategy if necessary,” says Buckingham.

1.Creating your strategy

When it comes to investing, the first – and most important – question to ask is simply, “Why do I want to do this?”

It’s a question many investors don’t seem to ask themselves until they’re well into the purchasing process, Buckingham says.

“When you ask people why they’re investing, many will respond with a vague answer like ‘to make money’ or ‘to have a property portfolio for retirement’,” he says.

The problem with answers like this is that ‘having money’ and ‘owning properties’ aren’t really goals per se.

They’re a means to an end but not an end in themselves.

“Investors without clear goals tend to approach their investing without a plan,” Buckingham says. “As a result, they often end up with portfolios that fail to meet their expectations and real financial needs.”

If your main objective is to create a recurring passive income, then income-producing deals such as positive cash flow properties could replace part of your salary.

Undertaking multiple similar deals might ultimately replace the entire income from your job over time. In this case, taking on longterm negatively geared growth properties may be counterproductive.

Alternatively, if your main goal is simply to have a lump sum of cash to buy the material things you want in life, then taking on a number of high capital growth properties or valueadding projects may be better suited to achieving this than positive cash flow investing.

To help narrow down the strategic choices available to you, Buckingham suggests taking a “path of least resistance” approach. With your overall goals in mind and an understanding of your current financial resources (available investing capital and borrowing capacity), consider what financial obstacles you are most likely to run into first. Are you more likely to exhaust your investing capital before you hit a borrowing limit, or vice versa?

If borrowing capacity is going to be the greater issue in the short term, then a strategy of investing in high-yielding positive cash flow property deals may boost your borrowing capacity and help you build your portfolio.

On the other hand, if limited investing capital is the greater constraint, then a strategy of actively adding value in order to rapidly add to your equity or capital base may make more sense than embedding all your existing capital into a positive cash flow property or longer-term growth investment at the outset.

You may even move back and forth between strategies over time, to help make your investing more sustainable.

2. Unlocking finance

With your strategy in mind, the next step is to secure finance for your prospective property. However, as Buckingham notes, it’s crucial to be well prepared when seeking a loan. Over the last few years, APRA (the main financial regulator of the banks) has been putting pressure on lenders to improve their ‘responsible lending’ standards. In tandem with the recent royal commission into banking and financial services, this has led to banks scrutinising how much a person can borrow much more heavily, with many taking a conservative approach around discretionary expenses.

“Stick to a tight budget for at least three months before your next loan application,” says Buckingham. “Obviously you’ll have fixed expenses, but it’s crucial to look at ways to cut back on discretionary expenses.”

Fixed expenses include rent or homeownership costs (eg mortgage payments, rates, home and contents insurance, utilities), school fees, childcare, ongoing medical costs, health and life insurance, and a reasonable allowance for essentials like groceries, transport, phone and clothing.

Discretionary expenses would include things like online subscriptions, gym memberships, wellbeing therapies (like naturopath or chiropractor appointments), dining out, charitable donations, or anything else that is perceived as being ‘easy’ to cut back on.

Buckingham also suggests minimising consumer debt as much as possible. Credit cards are one particular area in which caution should be exercised.

“It’s not the outstanding balance but the limit which impacts your borrowing capacity,” says Buckingham. “You should consider reassessing your limits, or possibly even eliminating certain cards altogether.”

3. Finding the right property

Finding the right property in the right area is intrinsically linked to your strategy. Being able to articulate a clear description of the type of property you’re looking for to real estate agents will immediately set you apart from other investors.

“Asking intelligent questions of the agent will encourage them to take you seriously,” says Buckingham. “If you go in and ask for a property that makes money, they’ll just tell you to get in line.”

Investors should also never buy based on emotional attachment or gut feeling, he says. Purchasing decisions need to be backed up by data and how effectively a new property would align with your overall financial objectives and related investing strategy.

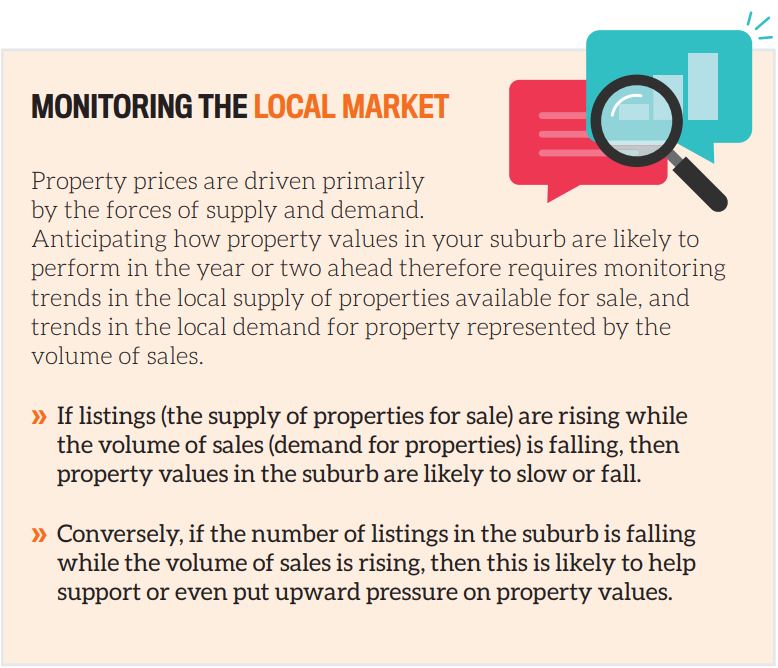

Buckingham explains that it’s perhaps most important to realise that, when selecting where and what to invest in, there isn’t a single, unified ‘property market’ in Australia. Each suburb is a market with its own dynamics, performing differently to the next. There are always suburbs where values are rising (or about to rise), while other suburbs are fl at or experiencing declining values. Rental yields also vary accordingly. Yet these facts are often obscured by an emphasis on median price movement. An emphasis on infrastructure or development is also often misguided, he cautions.

“At the end of the day, it’s about the buyers and sellers – it’s supply and demand like everything else,” says Buckingham. “Picking the right areas at the right time is closely related to looking at a particular suburb, then you look at the number of sales versus the number of listed properties, how quickly properties are selling, vacancy rates, rental yields, and the history of all these factors over the prior 12 months.”

There are many ways of making money from property. Some of these are more ‘passive’ in the sense that they require little ongoing effort – such as positive cash fl ow from rent, or market-driven capital growth. Others are more ‘active’, for example proactively adding value to a property through renovation, subdivision or development.

Neither approach is necessarily better than the other; they’re not mutually exclusive and you may use a combination of these approaches. For instance, if you have an income-oriented goal then you might focus fi rst on building up a capital base through growth properties and/or value-adding projects before ultimately reinvesting the equity created into high-yielding income properties. Alternatively, you might do a mix of growth, value-adding and cash fl ow properties as you go.

4. Negotiating amazing property deals

A smart investment strategy is to take advantage of current market conditions to secure great deals for yourself, Buckingham says. This requires a keen grasp of negotiation skills, and an ability to recognise the nature of the surrounding market.

“At the moment, we have a buyer’s market in many parts of the country, so that opens up negotiating opportunities that wouldn’t ordinarily be available,” Buckingham says. “Many buyers are hesitating, and sellers are more motivated – so it’s an ideal time to cherry-pick great deals in the right areas. We’ve seen some great examples of this recently, with some of our students achieving discounts of 10% or more off asking prices – even over 25% in some instances – through bold, clever negotiating tactics.”

There are some key points to remember when negotiating, he advises.

“You need to know how much you want to pay and why. You’ve got to understand your plans for the property and the numbers that would be involved. Never start with your best position either, because it leaves nowhere for you to go.”

He adds that negotiation isn’t simply about asking for price reductions.

“Depending on the property, you might look at other flexible terms – a long settlement, early access to the property, the current owner paying for certain renovations pre-settlement. It’s about getting a trade-off that keeps both you and the seller happy.”

Having objective data and independent standards to support your position is also crucial. Researching recent comparable sales, getting building reports and pest control assessments may require some investment of time or money but can end up saving you in the long run. “Last but not least, practise ahead of time with more experienced negotiators,” Buckingham says. “Going in unprepared is one of the worst mistakes to make.”

5. Establishing effective management

The process isn’t over after the property has been successfully purchased. Too many investors believe that their investing begins and ends with simply buying a property, Buckingham says.

“Once it’s handed off to a property manager, too many investors put very little thought or effort into the actual performance of the property.”

But actively reviewing and managing the property is essential, otherwise you increase the risk that the property may experience stagnant or declining values, increasing vacancies, rising costs, or cash flow issues.

“Even if the property has performed well in the past, the effective return may now have declined to the point where the property offers only a very ‘lazy’ return on investment, tying up capital or borrowing that could be better utilised elsewhere,” says Buckingham.

Failing to regularly review the performance of your property portfolio and take action to maximise this over time can mean that it takes far longer to achieve your financial goals. Worse still, issues may be present in your portfolio that, if left unaddressed, will actually work against the achievement of your goals.

It’s also important to regularly and proactively review the prevailing market conditions in the areas where you hold properties or plan to invest, to ensure that those market conditions are actually going to help rather than hinder the achievement of your financial goals.

“It doesn’t matter how many properties you have – having a clear understanding of each property’s performance is essential if you want to maximise your profits and arrive at your financial goals in the fastest possible time,” says Buckingham.

Securing future investments

There’s no need to panic if you’ve already spotted issues in your own portfolio after considering these five steps, Buckingham says. They are deliberately meant to be used as tune-ups and course corrections. Asking honest questions of yourself now will enable you to achieve better outcomes in the future.

“If you already have existing investment properties, take a moment to reflect on your current portfolio and assess whether your focus has been on capital growth or cash flow,” he says.

“Have you been active or passive in your pursuit of profits, and do you need to change your approach in the current market in order to achieve your financial goals?”

ABOUT RESULTS MENTORING

Results Mentoring is the home of Australia’s premier independent mentoring program for property investors seeking to achieve financial freedom through property: the RESULTS Mentoring Program – a multifaceted training and support program tailored to fit different learning styles and levels of investing experience.

.jpg)

Whether you’re getting started or are an experienced investor seeking to advance to the next level, Results Mentoring can provide you with the personal support, actionable strategies, intelligent investing techniques and in-depth information you need to profit from everyday property deals in any market conditions. To find out more, visit resultsmentoring.com or call 03 8843 7700.

EXCLUSIVE OFFER!

Results Mentoring is offering Your Investment Property readers a FREE Personal Property Investing Strategy Review with an expert property mentor.

To arrange your personal strategy session, register now at: resultsmentoring.com/strategy-call