The key figure to consider in planning your retirement income is your “total net investment assets”, excluding the family home, says Propertyology director Simon Pressley.

“Subtract your total liabilities from your total investment asset values,” he explains.

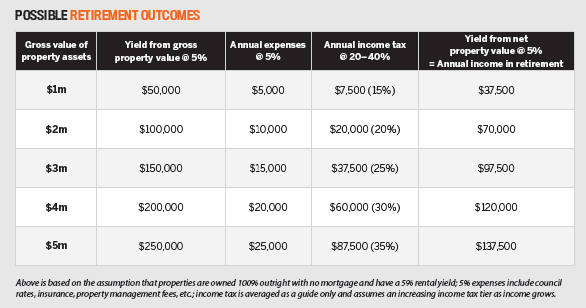

“For example, if you want a future retirement that includes a debt-free home plus $100k in annual income, you’ll need total net investment assets of $2m. For example, this might mean total investment property valued at $3m, less total liabilities of $1m, equalling $2m net – multiplied by 5% to get $100k per annum.

He advises that investors begin acquiring income-producing assets as early as they can in their lives, as the sooner you get started the longer you have for compounding interest to do its work.

“I’ve been privileged to help some people as young as 23 years old with their property investments,” he says.

Another benefit is that the longer you’re in the market, the more time you have to ride out down periods of low or no growth.

“Official data confirms that there are 111 individual Australian towns whose median house prices have at least tripled over the last 20 years, but it’s also common for there to be a stretch of seven to 10 years when values in each location don’t do much at all,” Pressley explains.

“Plant your seeds as early as you can. Once they start bearing fruit, plant those seeds early too. The aim is to grow an orchard capable of feeding your family in years to come.”

Striking a balance

If you want to purchase property for investment purposes, Pressley says a deliberate mental shift is required.

“People need to see property as a financial instrument,” he says.

For this reason, he recommends that property investors take a page out of a share investor’s book.

“Buying shares is a financial decision based on what has the best potential. So, if you’re investing in property, do it the same way. It should have nothing to do with where [someone] lives or whether they would like to live there, because that’s not how they are going to be using the property. We need to remove all of that personal bias,” Pressley says.

“It’s possible to invest for both capital growth and yield; there are no better examples over the last few years than in Hobart, Orange and Launceston”

He adds that, while you want to minimise debt and increase the income you are receiving from your investment properties, this shouldn’t be done at the expense of capital growth.

“We believe that it’s possible to invest for both capital growth and yield; there’s no better examples over the last few years than in Hobart, Orange and Launceston,” he says.

“Before investing, it’s prudent to stress-test personal cash flows by budgeting for rent 48 out of 52 weeks of the year, placing interest rate buffers, and setting aside a contingency fund of, say, $3,000 per property in your portfolio.”