Australia's top property investment experts unveil insider strategies for how to use investment property to pay off your home loan within 10 years. They reveal what, where, and how to buy to reap the rewards.

Owning your own home is something many of us aspire to, despite claims that homeownership is overrated. But let’s face it, most of us will carry our mortgage for at least 25 years before we can get rid of it.

Turns out you don’t have to. In this game plan, our experts lay out practical strategies for paying off your home loan sooner, using your investment property. They show you how to structure your finances, and what property to buy and when.

Philippe Brach's Strategy

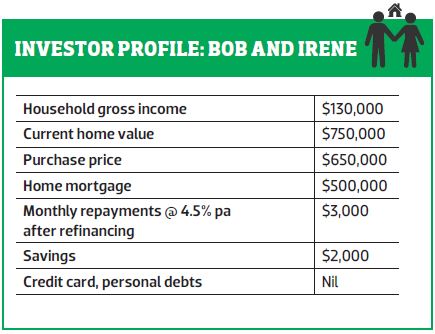

In this case study, Bob and Irene have an ambitious goal of paying off their mortgage in 10 years. They are currently paying $3,000 per month towards their mortgage, after refinancing.

Looking at it very simplistically, if they want to repay their mortgage in 10 years they need to increase their monthly repayments to $5,000 (assuming a 4.5% interest rate), which is an extra $2,000 per month. Obviously, this is not possible given the couple’s current circumstances.

They are wondering if they can somehow use the equity in their home to invest in an investment property with a view to helping them with their goal.

Many people think they need to fully repay their home loan before they can invest in property, so Bob and Irene’s line of thought is on the right track.

Borrowing capacity

Their current financial profile will allow them to borrow $540,000 to invest in property.

We could boost their borrowing capacity to about $750,000 by converting their home loan to interest-only repayments, as some lenders are happy to take actual repayments towards servicing.

However, this would be increasing the financial risk for the family, and I would not recommend this approach.

Using equity to invest

There is about $100,000 of equity in their home that can be used to help them acquire a property and still keep the overall loan-to-value ratio (LVR) below 80%, which is a LVR that most banks are comfortable with.

I would suggest accessing this equity by setting up a line of credit (LOC) of $100,000 secured by their home. LOCs are fully transactional accounts with a limit to spend. They’re a bit like a giant credit card but with home loan rates.

The LOC will be used to fund the deposit on the property, stamp duty, legal costs, etc.

A summary of the structure would be as follows:

Finding a property

I would suggest that our couple invest in a vibrant, up-and-coming location with substantial infrastructure spending, a multi-industry approach and strong population growth.

For the purpose of this case study, and to allow for a great property within Bob and Irene’s budget constraints, I have chosen a four-bedroom house and land package property in a great location in the Newcastle area.

This type of product is great for Bob and Irene because stamp duty only applies to the land portion of the purchase, and also because there is currently a $5,000 stamp duty rebate from the NSW government for new properties. This will substantially lower acquisition costs.

The property purchase price is $525,000 and the anticipated rent is $560 per week. This is higher than the average rent in Newcastle, but this property is ideally located by a sandy beach and can easily command such a rent. At a 6% interest rate, this property is cash flow neutral. So, in the current environment where interest rates are much lower, the property is cash flow positive.

Financing the property

As our couple has only $100,000 available in their LOC, thenew property will have to be financed by borrowing 90% of the purchase price. At 90%, lenders mortgage insurance (LMI) is applicable. LMI costs vary depending on the lender, but they are around $9,300. This one-off premium will be added to the loan and will increase monthly repayments by about $35.

The total amount that is needed to fund the acquisition is about $59,000, as shown below. This amount will be funded from the LOC.

Safety buffers

During construction of the house, interest will be payable on the amounts drawn and will add up to about $8,000 over the period of construction. Again, this will all be paid out of the LOC.

So by the time the property is ready to be tenanted, Bob and Irene will have used about $70,000 of their LOC. This includes interest on the LOC itself. As a result, they will have a $30,000 ‘buffer’, or unused funds, in their LOC when the first tenant moves in.

All rents collected, expenses (council rates, managing agent fees, interest on the investment loan, tax refund, etc.) are paid into or out of the LOC.

Since the property is cash flow positive, the balance of the LOC will decrease over time. If interest rates increase to 6% then the property wil be cash flow neutral and the balance of the LOC will remain the same over time.

The $30,000 buffer is designed for unexpected expenses and for peace of mind for Bob and Irene. In our case, our couple also has $20,000 in savings which they will keep for personal expenses. So they have two buffers, which should allow them to sleep soundly at night!

Avoiding cross-collateralisation

By structuring the loans in this manner, we avoid cross-collaterisation of the two properties, which is never advisable as it creates issues in the future, especially when trying to sell one of the properties or when refinancing. Banks love to cross-collaterise properties because it is easier to do and it makes it harder for the client to move to another lender. The client becomes a ‘sticky’ customer.

This structure also allows for the creation of a buffer, which is not only a good risk management tool but is also tax efficient (LOC interest is fully tax deductible) and allows for easy financial management of a property.

Capital growth expectations

According to BIS Shrapnel’s Australian Housing Outlook 2014–2017, the Newcastle area has grown by 10% in 2014 and is tipped to increase in value at a rate of 7% per annum over the next two years.

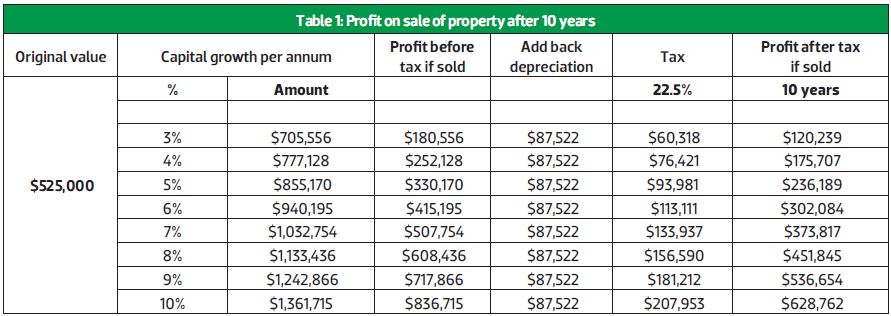

It is hard to predict what will happen beyond the short term. So investing in an area where the fundamentals are sound is the best we can do. At 7% growth, the property will almost double in value in 10 years. If the property is sold, capital gains tax will be payable, as shown in Table 1 below.

I have assumed that the tax rate is 22.5%, which is the highest rate for individuals who hold a property for over one year.

Fast-tracking repayments

At their current repayment rate, the balance of the home loan will be $330,000 in Year 10, assuming that the current interest rate on their loan remains at 4.5%.

As a result of the above, their loan balance will now be $228,400 in Year 10.

This means our couple could repay their home in Year 10 by selling the investment property, provided the property grows by about 5% per annum on average.

If interest rates go up during these 10 years, and there is a good chance that they will, then the numbers will look different. If we assume an average 6% interest rate over the 10 years, then the balance of their loan in Year 10 will be $305,600, and in order to repay their home loan our couple will need their investment property to grow by about 6%.

Further considerations

Although it is possible to use investment properties to repay home loans, investment properties are not ‘designed’ for that purpose. In this case study, the property helped to repay the home loan, but the homeowners had to increase their repayments to achieve the desired outcome.

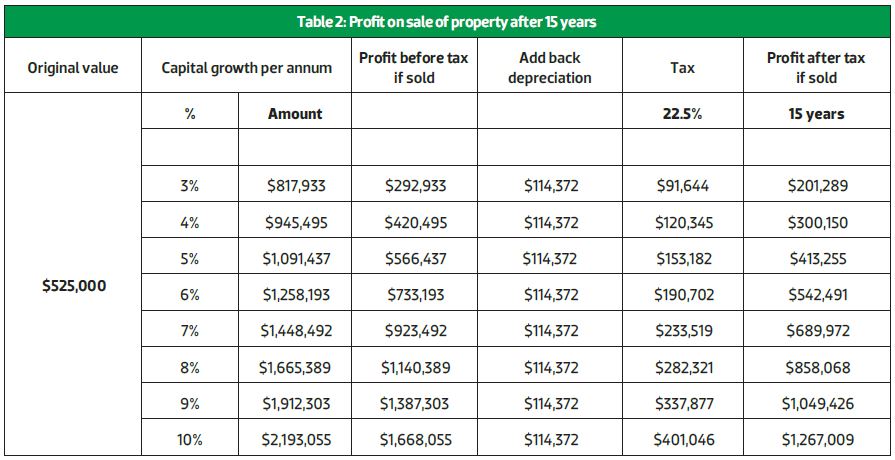

Growing wealth is all about planning, leverage and time. If Bob and Irene decided not to sell their investment property in Year 10 and keep it until Year 15, the results would be as shown in Table 2 below.

By keeping the property for a further five years – at 6% capital growth – profit would increase by 80%; and at 7% profit would increase by 85%. So Bob and Irene will need to decide if they should sell the property in Year 10 and repay their home loan, or keep it and grow their overall wealth. I know what I would do.

Ben Kingsley's Strategy

It’s an interesting concept that you can actually invest in property to help pay down your personal home loan sooner. The strategy I’m using to illustrate this is a passive investment strategy, meaning it won’t focus on any renovation or developing for profit.

It will be a buy-and-hold approach, focusing on taking advantage of the low interest rate environment and securing three cash flow positive properties. Then we will add the surplus cash flow into the offset or onto the actual mortgage to reduce the interest and accelerate the mortgage pay-down until there is no owner-occupier mortgage on the family home.

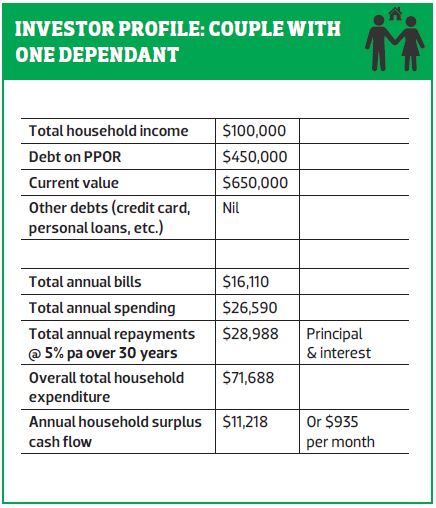

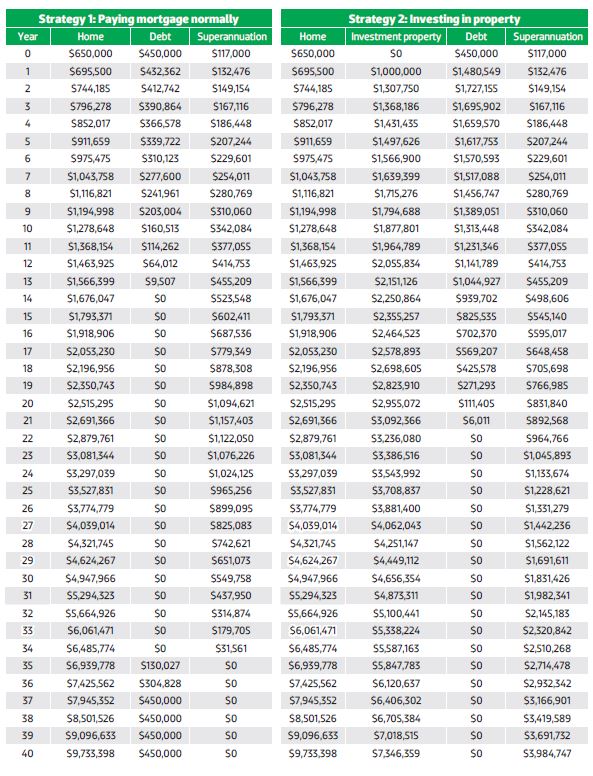

Before I show you my property recommendations, it’s important that we understand all the financial ‘numbers’ that are at play in this scenario. We have a couple with a home valued at $650,000 and a mortgage of $450,000. The couple has one dependent child, and we have assumed each parent is working, earning $50,000 gross each. There are no current investments and, importantly, no other debts.

Given this is an example household, we have had to make other assumptions about their financials.

Assumptions:

How mortgages work

For those new to understanding how mortgages are paid out over time, this means the household would make 360 monthly repayments over 30 years of $2,416 to pay this loan off, and also pay the interest amount every month over this period.

Therefore, if you pay extra on your mortgage or pool your surplus into an offset account, you can pay off the home loan sooner, as the interest calculated will be lower each month.

Using the numbers above, if the household was to apply the $935 per month in surplus onto the mortgage in this example, then the home loan would be paid down by March 2028, just over 13 years from now – pretty close to the 10-year target.

Furthermore, if we assumed the property would grow in value by 6% per annum, this household would be debt-free and the house would be worth $1.386m. Not bad at all. For the record, at the 10-year milestone interval this family’s household debt would be $153,000 and the property value would be $1.164m.

STRATEGY 1:

Paying off extra on the mortgage and using offset.

Why bother investing?

So, what is the benefit of trying to pay the home loan off within 10 years when by just paying extra on the home loan you can pay off the home loan in 13 years?

Well, besides the additional interest that you save over this three-year period, by paying your home loan off sooner, the much bigger benefit is in the property portfolio asset wealth and the ongoing passive income you are building up during this 10-year period.

This effectively means your money has worked harder for you than by just paying down your loan, and one could argue that by committing to this strategy the household becomes more focused on ensuring the surplus is maintained each month rather than being spent on discretionary items.

At the end of this article, I will reveal the asset value difference at the 10-year milestone interval so you can compare the two scenarios.

THE GAME PLAN

To secure more property, we need to borrow money from the bank, as we don’t have any cash savings in this scenario. We just have our equity, which is $200,000 – the difference between the value of the property and the mortgage balance.

The bank’s won’t let us use all this equity (nor should anyone seriously consider it), but in this property portfolio strategy build, we are going to have to use up to 90% of the equity in this property and across the portfolio initially as we build it out to meet the challenge of in 10 years having no principal residence debt.

It’s important to stress at this point that taking on higher debt does increase your financial risk, so do not try to replicate this example strategy without seeking advice from a qualified and licensed finance broker, as your circumstances more than likely will be very different from this illustrated example.

Once again, to best illustrate this example scenario, we need to document all the moving parts in terms of the variables and assumptions behind the ‘real’ numbers.

Assumptions

- Interest rate on all lending/borrowing at 5% over the 10 year period

- Household expenditure indexing at 3%

- Incomes increasing each year at 3%

- Rental occupancy of 95%

- Holding/maintenance costs of 1% of purchase price, then indexing at 3% per year

- All properties purchased in joint names-50/50 ownership of taxation calculations

- Purchase costs at 5% of the property values

- Property management fees of 7.7%

- Capitalisation of LMI onto new loans

With the above variables and assumptions in mind, and in determining the value of each investment property purchase, we need to be mindful of several other factors, such as the goal we are trying to achieve within the 10-year timeframe.

This means we need to accumulate as much value in the properties as we can, ensuring they are sufficiently positively geared and trying to limit any downside valuation risk, because more often than not most cash flow positive properties do carry higher volatility in terms of their valuation fluctuations.

PROPERTY 1

Purchase price: $550,000

Target yield: 6.5%

Annual growth target: 5%

Assuming:

Depreciation: $220,000 building write-downs

Fixtures and fittings: $35,000 write-downs

Timing: Immediately

I have led with a higher-value price point of $550,000, focusing on a good yield target of 6.5% and an annual growth target of 5%. In purchasing this property I have focused on some steady growth in addition to the cash flow focus.

Over time this will serve the investor well, as beyond the 10-year target this property will deliver a good mix of yield and growth. In addition, and in support of the cash flow focus, the property needs to have $220,000 in building depreciation and at least $35,000 in fitting and fixture write-downs. This property will be acquired immediately.

PROPERTY 2

Purchase price: $450,000

Target yield: 7%

Annual growth target: 4.5%

Assuming:

Depreciation: $170,000 building write-downs

Fixtures and fittings: $28,000 write-downs

Timing:6 months after first purchase

The second property will have a lower purchase price of $450,000, with a slightly higher yield target of 7% but a lower growth target of 4.5% per annum. I call this a yield-weighted property, whereby the yield/income is more important than the growth story.

By focusing on a lower price point, it makes it easier to find properties that offer this level of yield, as opposed to the higher-value properties where higher yields are harder to achieve unless it’s a remote or mining town location.

Once again I have factored in depreciation benefits – at least $170,000 on building write-downs and $28,000 in fitting and fixture write-downs. This property in my modelling would be acquired six months after the first property.

FINAL PROPERTY

Purchase price: $250,000

Target yield: 7%

Annual growth target: 4%

Assuming:

Depreciation: $135,000 building write-downs

Fixures and fittings: $15,000 write-downs

Timing: 6 months after the second property

The final property we need to acquire is a true little ‘cash cow’. At a purchase price of $250,000 this property is pretty much all about yield – at 7.5%, with the growth target at 4% per annum.

I’ve intentionally focused on a lower valuation on this purchase, because this is where you secure the higher-yield outcomes, and it is very much a yield play.

On the depreciation front I’ve factored in $135,000 of building write-down provisions and $15,000 worth of fixture and fitting write-downs. In terms of timing, this purchase would be made six months after the second property.

How the assumptions were made

In terms of the properties and the depreciation estimates I’ve used, they are consistent with properties that are about five years old.

The couple would need to acquire three properties in relatively quick succession – each different to the other and each serving a purpose in providing improved monthly household cash flow surpluses to get the home mortgage down more quickly.

My modelled result tells us that the principal home loan will be paid off in just under 10 years with the above property portfolio plan, and factoring in all the detailed variations and assumptions that are ‘real’ factors in testing the numbers and the possibility of this scenario working.

STRATEGY 1: Paying extra to the mortgage, investments

If our pure focus was to pay off the mortgage in 10 years, with just the monthly surplus we would end up with a debt of $153,000 remaining against an estimated property valuation of $1.164m.

AFTER 10 YEARS

Total debt against the home: $153,000

Home value: $1.164m

STRATEGY 2: Investing in three properties

Year 1

Total debt: $1.3m

Total property portfolio: $3.213m

AFTER 15 YEARS

Debt: Nil

Passive income: $209,400 pa

Total value of properties: $5.878m

In our new scenario we have no personal mortgage against our owner-occupier home, but we do have deductible investment debt of $1.3m against an estimated total property portfolio of $3.213m.

The modelling illustrates an over $900,000 improvement in wealth after 10 years, and as time moves forwards the total investment debt will be paid off by May 2036, at which time our modelling indicates the passive income being generated by these three rental properties will be $209,400 (in future-value terms). Even more impressive is that the total value of all their properties is projected at $5.878m.