Q: I bought a house for $300,000 (House A) in January 2003 and lived there for five years. Then I bought another house for $450,000 (House B), moved in January 2008 and started to rent out House A from that date forward.

Ten years later, in 2018, we went back to live in House A and started to rent out House B on the same date that we moved back.

My questions are, if we sell House A for $700,000, how do we calculate its capital gains tax? If we sell House B on 1 June 2020 for $750,000, how do we calculate the capital gains tax for this?

Regards, Don

A: As per the Australian Taxation Office (ATO), your main residence is generally exempt from capital gains tax (CGT). In order to be exempt, you must have resided in a dwelling on said property.

However, you can still continue to treat a property as a main residence after you’ve moved out – if the property has been used to produce income, then it can still be considered your main residence for up to six years. This is known as the six-year absence rule.

A special rule under section 118.192 of the Income Tax Assessment Act 1997 allows a reset of the cost base of a main residence to the market value when the property was first used to produce income. Effectively, you are taken to have acquired a property at its market value, and all costs incurred prior to that first rental date are ignored.

The cost base of a main residence must be reset to its market value when the property was first used to produce income

Given that you have two properties that are each eligible for election as your main residence for CGT purposes, you have the following options to consider.

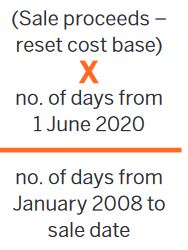

1. For House B, you can choose to apply the six-year absence rule to extend from 2018 when you moved out to the time of sale on 1 June 2020. In this case, the full CGT on the sale of House B would be exempt as it would be fully covered under the main residence exemption. For this purpose, you would then ignore any time you lived in House A from 2018 to the time of sale of House B as you cannot have more than one property elected as your main residence for the same overlapping period.

House A would then be taxed on a pro rata basis as follows:

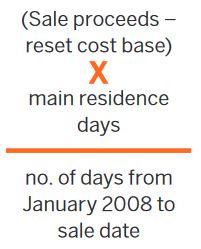

2. Instead of applying the absence rule to House B, you can choose to treat House A as your main residence for CGT purposes, to include your absence and the period after you moved back in. The cost base of House B is then taken to be its valuation at 2018, when the property was first used to produce income. Any costs prior to 2018 are ignored in this case. Thus, the CGT on House B will be based on the difference between the sale proceeds and the reset cost base.The CGT on House A would then be calculated on a pro rata basis as follows:

You can elect which property to use as your main residence for the overlapping period when you lodge your tax return in the year you first sell either property.

Need to know

- You can elect only one property at a time as your main residence.

- You must reset its cost base to the market value on the date it is first used to produce income.

- You only need to elect a property as your main residence when you file your tax return in the year the property is sold.

Lilian Fisher

Lilian Fisher

is partner at

Chan & Naylor Perth

If you would like your tax question answered in our magazine or on our website, please email your question to: editor.yipmag@keymedia.com.au