There’s been a debate raging for many years, which is better: time in the market; or timing the market? “Time in” the market is all about patience. If you wait long enough, eventually capital growth will come. Alternatively, “timing” the market is all about picking when you buy.

- Time in > Wait > Hold >Long-term

- Timing > When >Trade >Short-term

Pros & Cons

Advantages of Holding

Great for those with time on their hands like young investors.

Disadvantages of Holding

Some markets have been flat for decades.

Advantages of Trading

Timing entry into the market gives the investor equity to reinvest sooner, getting compounding to work earlier.

Disadvantages of Trading

The big problem with trading property is the high entry and exit costs.

The big question

Is an investor better off selling at the start of a period of flat growth and invest elsewhere, or should they hold on?

Selling and re-buying is expensive. Where will you re-allocate your proceeds from the sale? Will it be much better?

Examples

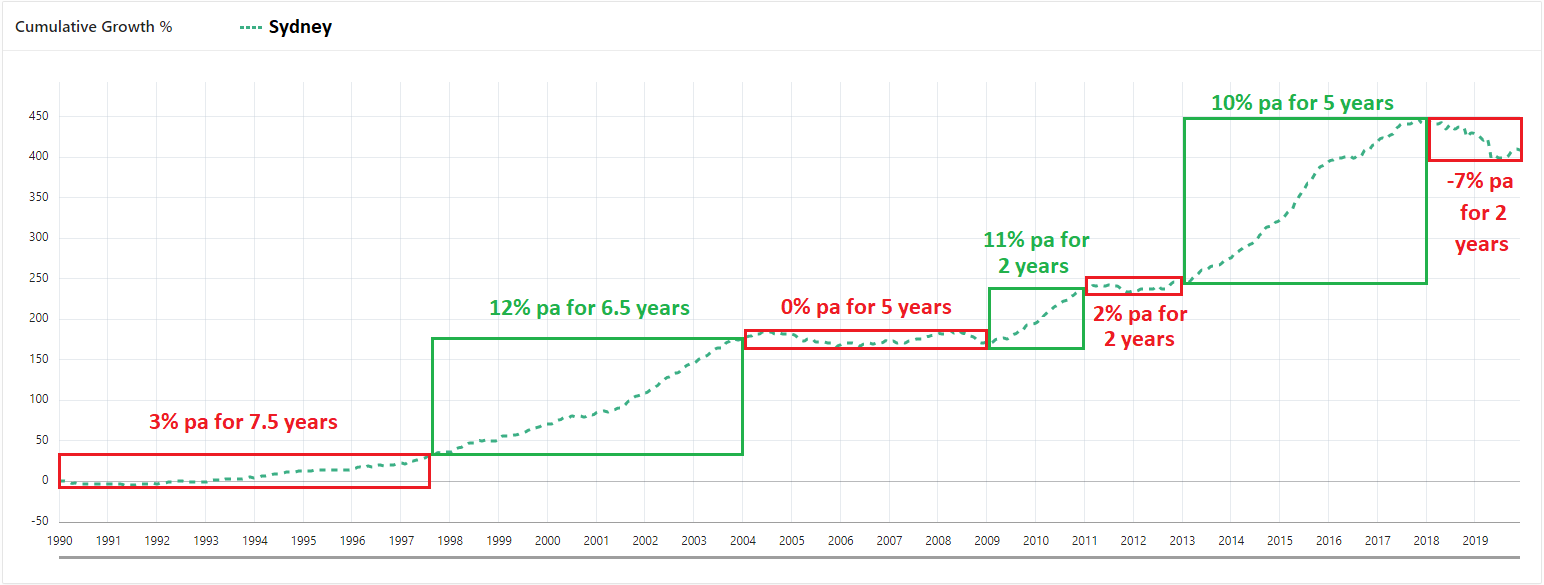

In the last 30 years Sydney has spent more than half its time with a growth rate on par with inflation.

There have really only been three periods where ownership of property in Sydney has been worthwhile over the last 30 years.

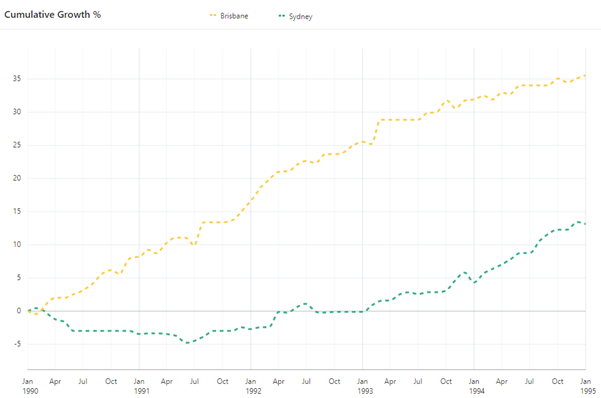

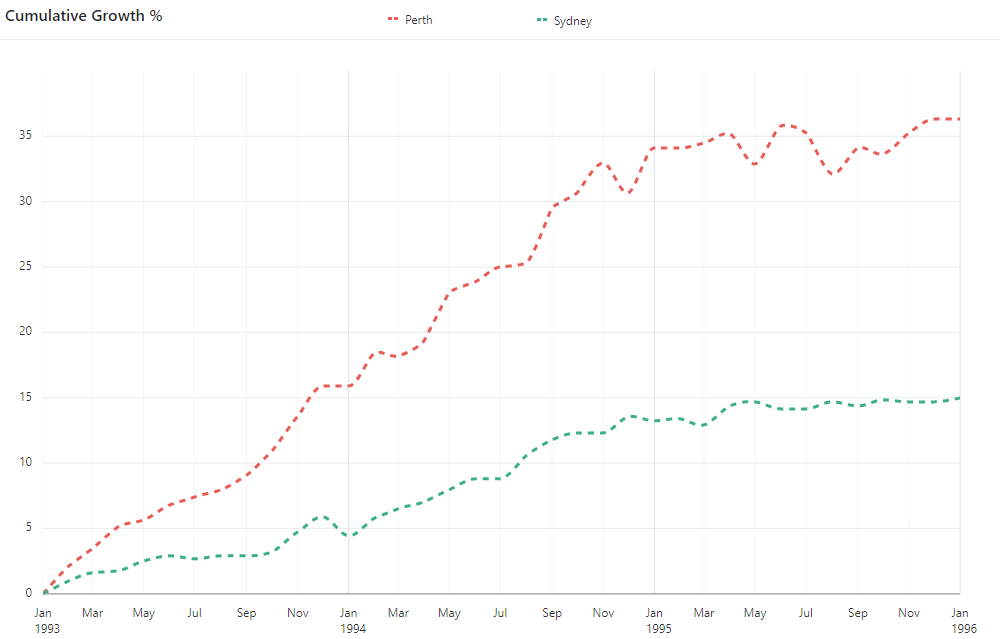

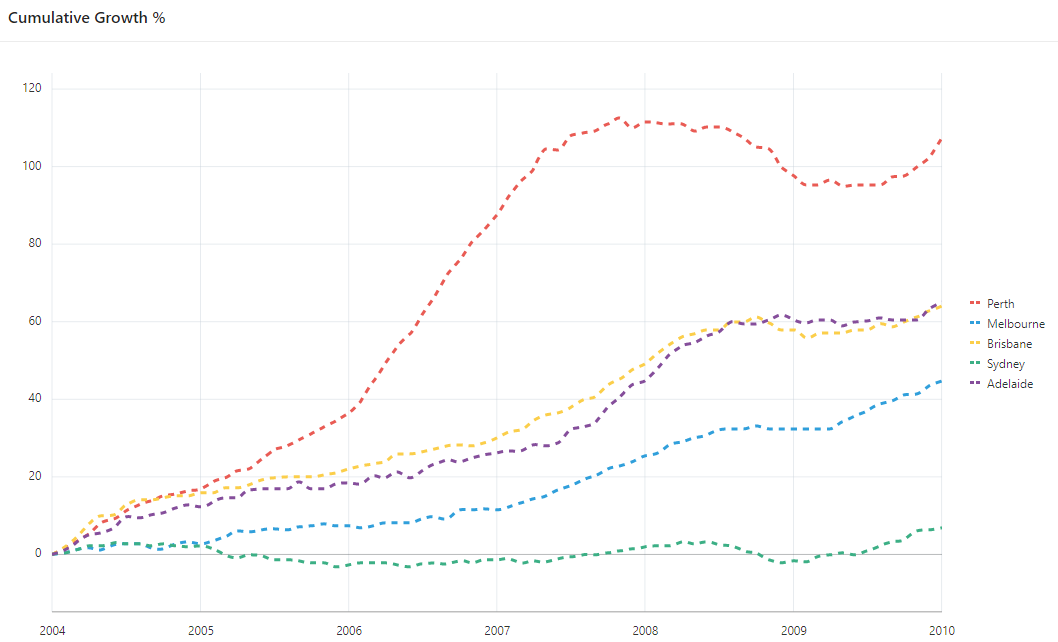

While Sydney was having those poor growth periods (red), other cities were booming.

Brisbane had more than double the growth that Sydney did. And from 1993 to 1996 Perth had more than double the growth of Sydney.

And from 2004 to 2010 there were 4 major cities that had good/great growth while Sydney was stagnant.

But these are just examples.

Last 10 years growth

I came up with a simple trading algorithm based on the past ten years of growth to see if now is the right time to buy or sell. It’s based on a metric called the Long-Term Growth (LTG). The LTG is the per annum growth rate for a suburb over the last 10 years.

- LTG = Long-Term Growth

- % p.a.

- Last 10 years

This algorithm is not something I’ve ever used nor would advocate investors to use. I’m simply checking to see if using it to trade property would be better than holding long-term.

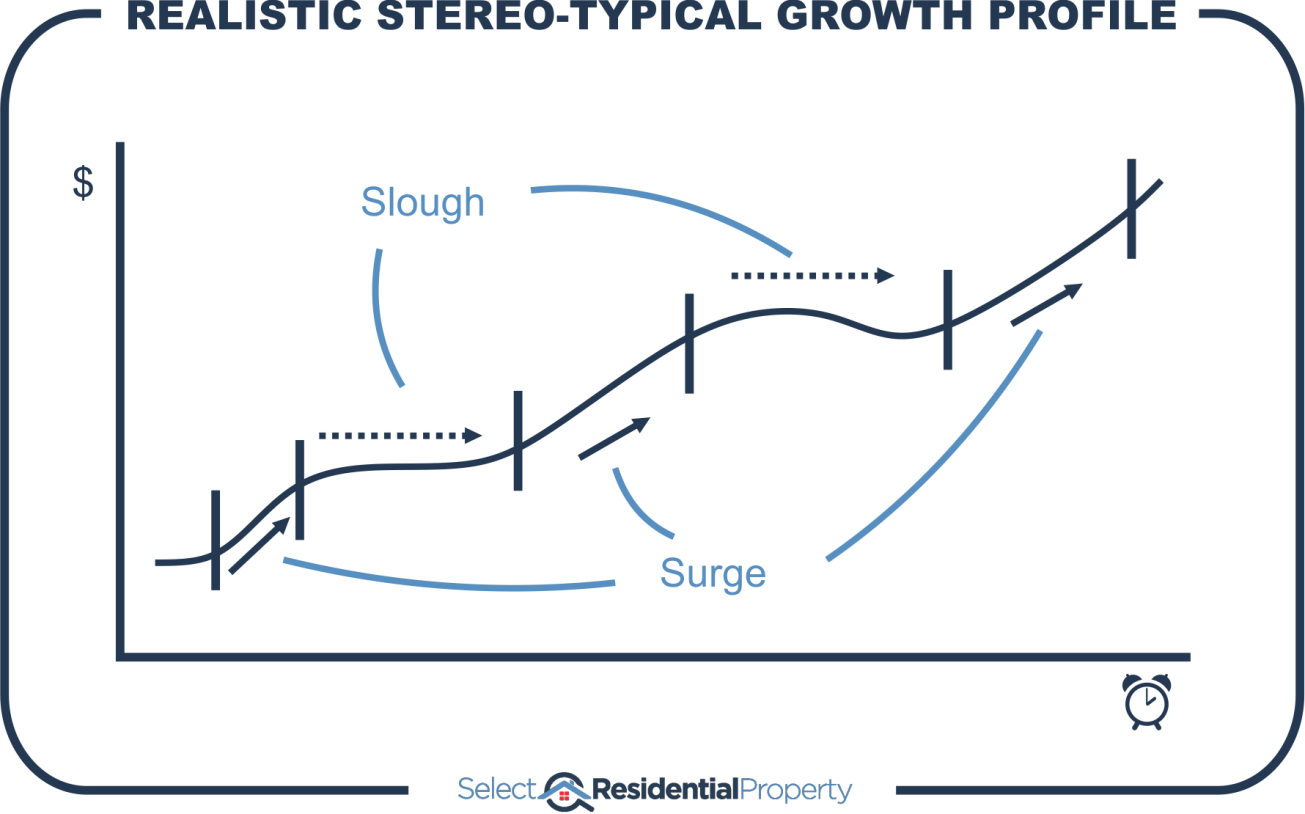

Towards the end of a suburb’s boom, higher prices start to push buyers away. This subdues demand such that further price rises slow and eventually stop.

This surge and slough cycle can easily extend beyond ten years, so it’s a hell of an assumption to make. But since I have LTG data dating back decades, it’s one metric I can examine over the long term.

Timing with historical growth

I came up with a very simple set of rules to pick a market to buy and when to sell:

- BUYING RULES:

- Find a market with an LTG as close as possible to 3% pa. Why:

- a low LTG identifies markets possibly due for a growth surge

- LTG must be between 0% pa and 6% pa Why:

- ignore danger markets (LTG < 0%)

- ignore markets that may have boomed recently (LTG > 6%)

- Growth last 9 months of more than 4%. Why:

- Find markets showing recent green shoots of growth

- 6 months is a bit too soon to say for sure a growth surge is starting

- 12 months is a bit too late to react to the new growth surge

- Find a market with an LTG as close as possible to 3% pa. Why:

- SELLING RULES:

- Growth last 12 months less than 6% pa. Why:

- growth rates are starting to slow below long-term national avg.

- But don’t sell within 3 years. Why:

- Give it a chance

- Good growth surges aren’t usually shorter than 3 years

- LTG is not an immediate growth indicator

- If growth didn’t come, exit quickly and try again elsewhere

- And always sell after 5 years. Why:

- 5 or 6 years should be enough time to capitalise on the growth spurt

- If there wasn’t one, exit and try again elsewhere

- We don’t want to wait forever to eventually be proven right

- Admit the mistake, exit early and move on

- Growth last 12 months less than 6% pa. Why:

This is an extremely crude investment algorithm. If timing is so hard, it should not be this easy to outperform holding long-term.

A couple more rules

- Houses only, not units

- At least 48 sales per year

- Calculate growth at the SA4 level (region) not suburb level

Suburb vs. SA4

SA4 is short for Statistical Area Level 4, defined by the Australian Bureau of Statistics.

- SA4 – like a region

- SA3 – like a local government area (council)

- SA2 – like a suburb

- SA3 – like a local government area (council)

January 2000

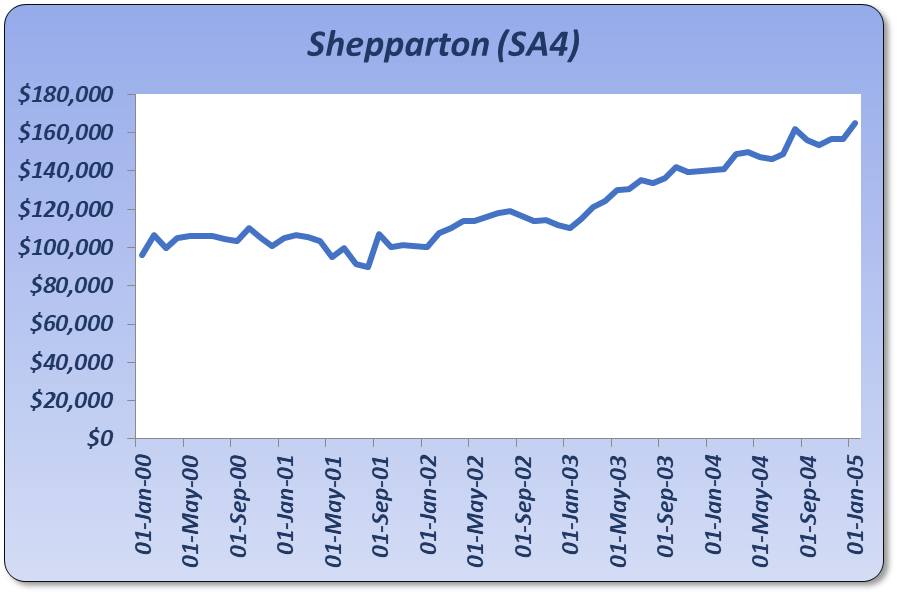

The first SA4 the algorithm picked in January 2000 was “Shepparton”. I had nothing to do with this, it was the algorithm that picked it.

|

Region |

Buy mth |

Buy val. |

LTG at start |

Recent growth % tot. |

Sell or end mth |

Sell or end val. |

Years owned |

LTG at sale |

Cap. Gro. % tot |

Buy costs |

Sell costs |

CGT |

Post- tax gain |

Compound gain % |

|

Case 1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shepparton |

Jan-00 |

$94k |

2.7% |

14.6% |

Feb-03 |

$114k |

3.1 |

4.8% |

20.7% |

$3.8k |

$2.8k |

$2.6k |

$10k |

11% |

The median value in January 2000 for the Shepparton SA4 was $94,000. The LTG was 2.7% which is close to our target of 3%. Recent growth over the 9 months leading up to January 2000 was 14.6%. This satisfied our buying rules.

Using our selling rules we would have sold out of the Shepparton SA4 just over 3 years later. By then the median had risen to $114,000.

To calculate a net gain, we need to consider entry and exit costs. It cost us $3,800 when we bought. This was the total of: stamp duty, legal fees and inspections.

The sale in Feb 2003 cost us $2,800 which was mostly the agent’s commission. That didn’t include CGT which was another $2.6k = ($114k - $94k - $3.8k - $2.8k) x 50% CGT discount x 40% marginal tax rate.

All up, we only made $10k after tax. As a percentage of the original purchase price, it’s a measly 11% which is pretty bad for 3 years.

Note that I have excluded rental income, holding costs and depreciation from calculations for a couple of reasons. Firstly, they’re going to work out to be very similar to holding long-term anyway. Secondly, it simplifies the modelling. But most importantly, they’re insignificant compared to the differences in capital growth between trading and holding long-term. Taking net cash-flow into consideration would open up even more alternative markets to choose from, some with better net yields.

The growth chart of Shepparton medians shows the market didn’t respond as we expected.

The SA4 was quite sluggish for the first 3 years. But then prices took off – just after we sold! Holding on a little longer would have proved very fruitful. This is a case where the simplicity of the algorithm worked against us.

Note that we’re not buying a specific house in a specific suburb of Shepparton. These performance calculations are based on the average for the SA4.

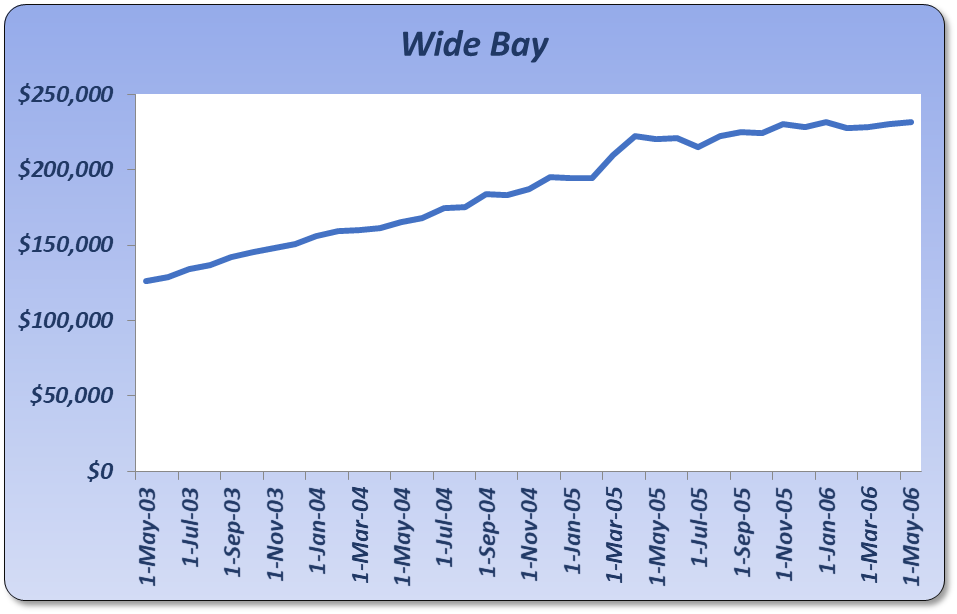

After selling out of Shepparton in Feb 2003, the algorithm told us to buy again a few months later (May 2003) in a Queensland SA4 called, “Wide Bay” which is around Bundaberg.

|

Suburb |

Buy mth |

Buy val. |

LTG at start |

Recent growth % tot. |

Sell or end mth |

Sell or end val. |

Years owned |

LTG at sale |

Cap. Gro. % tot |

Buy costs |

Sell costs |

CGT |

Post- tax gain |

Comp- ounded gain % |

|

Case 1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shepparton |

Jan-00 |

$94k |

2.7% |

14.6% |

Feb-03 |

$114k |

3.1 |

4.8% |

20.7% |

$3.8k |

$2.8k |

$2.6k |

$10k |

11% |

|

Wide Bay |

May-03 |

$130k |

3.0% |

13.0% |

May-06 |

$230k |

3.0 |

9.0% |

76.9% |

$5.2k |

$5.8k |

$18k |

$71k |

72% |

The rightmost column takes the gain from the last trade (which was 11%) and compounds it with the gain of the most recent trade to give a total cumulative compounded gain of 72% after 2 trades. That’s not 72% for the Wide Bay property, it’s 72% overall for both Shepparton and Wide Bay trades:

- First trade: $10k as a percentage of $94k = 11%

- Second trade: $71k as a percentage of $130k = 55%

- ((1 + 0.11) x (1 + 0.55)) - 1 = 0.72 or 72%

Some of the dollar figures have been rounded to the nearest thousand.

Remember that a doubling in value is the same as multiplying by 2 which is the same as growing by 100%.

Here’s how the SA4 performed over those 3 years.

Now things are looking pretty good.

There were 3 more purchases to bring us to the end of 2019 (time of writing).

|

Suburb |

Buy mth |

Buy val. |

LTG at start |

Recent growth % tot. |

Sell or end mth |

Sell or end val. |

Years owned |

LTG at sale |

Cap. Gro. % tot |

Cap. Gro. % pa |

Buy costs |

Sell costs |

CGT |

Post- tax gain |

Comp- ounded gain % |

|

Case 1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shepparton |

Jan-00 |

$94k |

2.7% |

14.6% |

Feb-03 |

$114k |

3.1 |

4.8% |

20.7% |

6.3% |

$3.8k |

$2.8k |

$2.6k |

$10k |

11% |

|

Wide Bay |

May-03 |

$130k |

3.0% |

13.0% |

May-06 |

$230k |

3.0 |

9.0% |

76.9% |

20.9% |

$5.2k |

$5.8k |

$18k |

$71k |

72% |

|

Sydney - Inner South West |

Nov-09 |

$565k |

5.8% |

4.6% |

Nov-12 |

$696k |

3.0 |

3.9% |

23.2% |

7.2% |

$23k |

$17k |

$18k |

$73k |

94% |

|

Sydney - South West |

Feb-13 |

$475k |

3.3% |

5.5% |

Nov-16 |

$755k |

3.7 |

7.3% |

58.8% |

13.1% |

$19k |

$19k |

$48k |

$193k |

173% |

|

Hobart |

Feb-17 |

$383k |

3.0% |

4.9% |

Dec-19 |

$507k |

2.8 |

|

29.0% |

9.5% |

$15k |

n/a |

n/a |

$109k |

251% |

Note that it takes time to sell a property and sign a contract for a replacement. This is included in the model. In fact, there were some periods where we couldn’t find a suitable replacement – nothing satisfied our buying rules. When the algorithm sold out of Wide Bay in May 2006 it bought in “Sydney – Inner South West”. But it took till November 2009 for that case to appear. There was nothing else that satisfied our buying rules.

Also, note that there was no time for a final sale of the last SA4, “Hobart”. It was only held for 2.8 years. So, for this last purchase the selling costs are not deducted and show up as “n/a” in the table. But there has been some equity gain, so this is added to our total compounded gain of 251% shown in the last cell in the bottom right of the table.

Let’s compare this trading performance with holding long-term.

Comparisons

If we held onto Shepparton for the full term of twenty years, values would now be around $257,000. That’s a gain of 169%. But “trading” in and out of SA4s gave us over 251%. But it’s still a failure because the growth on average for any property market in Australia for that 20-year period was 279%.

Following is a summary of the performance comparison of this trading case against some more popular benchmarks:

- Trading > 251%

- Trading outperformed

- Holding > 169%

- Trading underperformed

- National average > 279%

- Sydney, Melbourne & Brisbane average > 298%

- Syd, Mel & Bris within 10km of CBD average > 331%

- Best significant urban area (Hobart) > 402%

- Best SA4 (Mornington Peninsula) > 450%

Overall, this trading case was a failure. It was beaten by almost every benchmark. But we need to examine more cases to be sure this LTG algorithm sucks.

Repeat cases

I re-ran the algorithm over the same time-frame with instructions not to select Shepparton, but to start with the second best SA4 instead. Case #2 had a very different end result with a total compounded gain of 560% - more than double the first case! Following are the trades in case #2.

|

Suburb |

Buy mth |

Buy val. |

LTG at start |

Recent growth % tot. |

Sell or end mth |

Sell or end val. |

Years owned |

LTG at sale |

Cap. Gro. % tot |

Cap. Gro. % pa |

Buy costs |

Sell costs |

CGT |

Post- tax gain |

Comp- ounded gain % |

|

Case 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Sydney - Outer West and Blue Mountains |

Jan-00 |

$173k |

3.4% |

15.5% |

Jan-05 |

$355k |

5.0 |

11.0% |

104.6% |

15.4% |

$6.9k |

$8.9k |

$33k |

$132k |

76% |

|

Queensland - Outback |

Apr-05 |

$122k |

4.0% |

11.1% |

Jan-10 |

$302k |

4.8 |

11.3% |

147.3% |

21.0% |

$4.9k |

$7.6k |

$34k |

$134k |

270% |

|

Sydney - Sutherland |

Apr-10 |

$685k |

5.7% |

8.5% |

Apr-13 |

$760k |

3.0 |

3.2% |

11.0% |

3.5% |

$27k |

$19k |

$5.8k |

$23k |

283% |

|

Sydney - Inner South West |

Jul-13 |

$740k |

3.1% |

6.3% |

Aug-16 |

$1.1m |

3.1 |

7.6% |

46.8% |

13.2% |

$30k |

$27k |

$58k |

$232k |

402% |

|

Hobart |

Nov-16 |

$385k |

3.0% |

6.6% |

Dec-19 |

$521k |

3.1 |

|

39.6% |

11.4% |

$15k |

n/a |

n/a |

$121k |

560% |

Here are the comparisons:

- Trading > 560%

- Trading outperformed

- Holding > 271%

- National average > 279%

- Sydney, Melbourne & Brisbane average > 298%

- Syd, Mel & Bris within 10km of CBD average > 331%

- Best significant urban area (Hobart) > 402%

- Best SA4 (Mornington Peninsula) > 450%

- Trading underperformed

- Nothing

At this stage we’ve got one fail and one success for this algorithm. I repeated this process again several times. Each time I told the algorithm to ignore the best SA4s from earlier cases. I repeated this 20 times. Here are the comparisons averaged out over all 20 cases:

- Trading average > 496%

- Trading outperformed

- Holding > 310%

- National average > 279%

- Sydney, Melbourne & Brisbane average > 298%

- Syd, Mel & Bris within 10km of CBD average > 331%

- Best significant urban area (Hobart) > 402%

- Best SA4 (Mornington Peninsula) > 450%

- Trading underperformed

- Nothing

There was only 1 case out of 20 where the trading algorithm failed to beat holding long-term – the 1st case. And the average performance was better than the best performing SA4 in the country over that time-frame. Pretty impressive for an algorithm that uses only one metric.

More testing

Just to make sure there wasn’t something special about January 2000, I repeated the 20 test cases starting from June 2000 instead of January 2000. Summarising all 20 cases:

- 100% of trading cases outperformed holding long-term

- Average trading performance > 501%

- Average holding performance > 295%

- All Australia average performance > 264%

- Sydney, Melbourne, Brisbane combined > 283%

- Sydney, Melbourne, Brisbane combined within 10km of the CBD > 313%

- Best performing state capital (Hobart) > 387%

- Best performing significant urban area (Hobart) > 387%

- Best performing SA4 (Mornington Peninsula) > 397%

Not a single long-term hold benchmark managed to outperform trading.

That’s two time periods tested: from January 2000 and from June 2000. I repeated the process again for January 2001. The results were again very impressive with a 95% success rate. And for June 2001 it was once again the same story.

Last 15 years

I tested the algorithm again from 15 years ago (i.e. 2005) rather than 20 years ago. However, the algorithm could only find 7 cases that matched our buying rules at that time, so I couldn’t test over 20 cases. But all 7 were a success.

Summarising

Summarising the benefits of timing the market:

- Accumulate a safety margin more quickly in case you’re forced to sell too soon

- Leverage from gains sooner to start compounding sooner with next purchase

- You don’t know how long you’ll have to wait with the long-term hold approach

- You may have a short horizon, e.g. if you’re nearing retirement

- You may be able to “trade” property by timing your exit too

- Better data now days making even simple algorithms more successful than holding

- More frequent value-adding opportunities

Conclusion

As you can see, applying a trivial trading algorithm can outperform holding long-term. And if we were to add more metrics and refine it further, we could expect even better results.

BTW, if you get the entry timing wrong, just fall back on the “hold long-term” approach.

....................................................................................

Jeremy Sheppard is head of research at DSRdata.com.au.

Jeremy Sheppard is head of research at DSRdata.com.au.

DSR data can be found on the YIP Top suburbs page.

Click Here to read more Expert Advice articles by Jeremy Sheppard

Disclaimer: while due care is taken, the viewpoints expressed by contributors do not necessarily reflect the opinions of Your Investment Property.