Our property markets are in the headlines every day, aren’t they?

While many commentators are calling our current property market a “boom”, some are already suggesting we in a “property bubble?”

Just look how the economists from all our major banks have now done an about face and agree that we’re in for strong property markets for the next few years.

In fact, they seem to be outdoing each other to see who can come up with the most upbeat price increase forecasts.

Six per cent gains? How about 8 per cent? No, it will be double digit growth.

CBA suggested 16 per cent property price growth over the next two years.

Now Westpac went one better and forecast 20 per cent price growth over the next 2 years.

So to get a better understanding of what’s ahead for our property markets let’s do a little Q&A:

What’s the difference between a housing boom and a bubble?

Our property markets, like the economy, move in cycles with the property boom (when property values rise strongly) usually being the shortest phase at the end of the cycle.

Property booms eventually run out of steam and end in a small price correction.

On the other hand, by definition, bubbles burst and house prices end up much lower than where they started.

The good news is that bubbles don’t really happen in the general Australian property markets which are underpinned by a large proportion of owner occupiers.

However in the past we have seen bubbles occur in certain speculative sectors of the property market such as mining towns or off the plan, poor quality high-rise apartment towers in our capital city CBD’s

Why are housing prices rising so fast?

Currently property values are rising around Australia because buyers and sellers have re-entered the market buoyed by historically low interest rates, the assurance from the RBA that interest rate won’t rise for three years or so and increasing consumer confidence that we’ve got the coronavirus “thingy” under control.

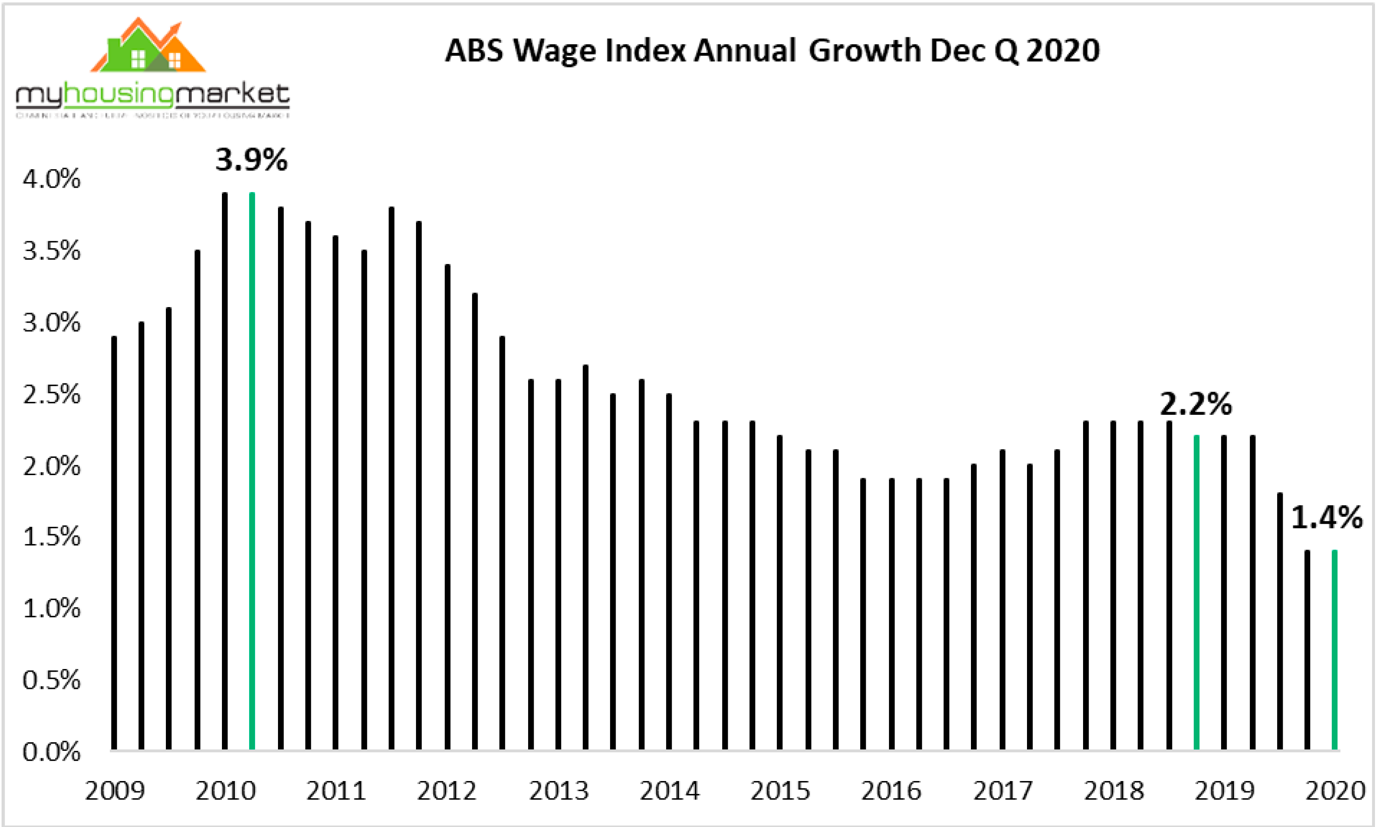

If you think about it, our property markets have been constrained since 2017 and prices are only now once again at the levels they were in 2017 in both Melbourne and Sydney, yet in that time we have had wages increase of up to 6% and interest rates have dropped 1%.

In other words, properties are more affordable now than they have been for a long time and currently our markets are being driven by owner occupies who see good value in the market, rather than by investors who are returning to the market more slowly.

What we’re seeing is pent-up demand from home buyers catching up for those lost few years.

To make things worse, currently there is a supply demand imbalance, with the strong demand not being matched by the number of new listings of dwellings for sale.

Currently around Australia there is around two and a half months’ worth of properties on the market – a sign of low inventory while there is normally there is more like four months of “inventory” available for sale.

What will happen to property values in 2021?

It is likely the confluence of multiple growth drivers will lead to continued property price rises in 2021 and 2022 but then once we absorb the catch-up demand in the market, property price growth is likely to slow down.

A leading indicator of future price growth is housing finance approvals, and at the end of last year we saw a big boom in lending – up 40% to the end of the year from the very low levels.

While average capital city home prices are likely to rise by around 10% this year and a little less next year, making such broad-brush statements can be misleading.

It is likely that houses will outperform apartments, and while currently all segments of the market are performing strongly, higher end, more expensive properties are likely to outperform the cheaper segments of the market.

Investor interest is already picking up, and as they return to the market, as they always do as the cycle moves on, this will extend the length of our property price boom.

Which sectors of the property market will outperform?

One of the trends we saw during Covid was that the rich kept getting richer.

While general wages growth will remain slow moving forward, there are some sectors of our economy that are performing strongly and knowledge workers, professionals and other skilled highly paid workers are still seeing strong and rising demand for their talents and enjoying rising wages.

This will lead to a two-tiered market with established money, more affluent inner and middle ring suburbs outperforming blue collar suburbs.

At the same time the city high-rise apartment market will languish since both investors and owner occupiers are steering clear of the many Lego Land apartment towers where rents have plummeted and values have fallen significantly.

What will happen to the boom in First Home Buyers?

Currently the influx of first homebuyers in the market is due to the federal government’s First Home Loan Deposit Scheme, along with HomeBuilder, stamp duty savings and other state-based incentives.

These time sensitive incentives have brought forward future demand which means the number of homebuyers entering the market over the next year or two, once the incentives finish, will be lower.

Are there any other obvious trends?

This is a period with many Australians that are upgrading their accommodation.

- Tenants who are unhappy with their accommodation are upgrading to better tenancies.

- Other tenants you’ve got a bit of money behind them and can take advantage of the government grants and incentives are upgrading and becoming first homebuyers.

- Established homebuyers can see property prices surging and many are looking to upgrade their homes to bigger or better accommodation in better locations.

- Other homeowners are upgrading to lifestyle locations and

- Some baby boomers are upgrading their lifestyle by downgrading their homes to larger apartments or townhouses in desirable neighbourhoods.

What could slow down or stop property price growth?

Of course a major factor that could slow down our property markets would be a resurgence of the coronavirus causing economic turmoil, but this now seems unlikely.

To a lesser degree, as the vaccine rolls out, if we keep experiencing uncertainty due to constantly changing interstate border restrictions this would lead to uncertainty across the property markets.

While there is already talk of regulatory intervention to slow down our housing market through changing lending criteria or rising interest rates, I don’t see either of these happening in the next 2 to 3 years.

But here’s what I think will eventually slow down this market….

As property values are dictated by affordability, moving forward in this period of low wages growth, it is likely that by the middle of next year our property boom will be slowed down by rising prices at a time when borrowers won’t have the capacity to keep going back to the bank and borrow more money.

Despite the strong recent labour market rebound, wages growth remains at record low levels.

Source: Dr. Andrew Wilson, My Housing Market

Source: Dr. Andrew Wilson, My Housing Market

One of the major factors leading to price growth over the last decade has been falling interest rates (making finance cheaper) and rising wages (increasing the ability to service loans), but clearly these drivers will be absent moving forward.

Recently regional property prices have risen at nearly double the rate of capital cities, in part due to the newfound popularity of regional housing options, but this trend is also likely to lose steam as life becomes more normal post Covid19.

While there’s no doubt some people are moving to regional locations close to the CBD, you just have to go to any open for inspection in any capital city or attend any auction and you’ll see that the bulk of the buyers still want to live in the big smoke.

Finally, low levels of international migration will impact the level of new developments coming out of the ground.

The bottom line…

We are at the early stages of a new property cycle and the current mix of increasing consumer confidence and pent-up demand at a time of historically low interest rates, easy finance and a plethora of government incentives is causing the current surge in owner-occupier housing demand.

But when the new affordability ceilings are reached, growth will slow down, but it won’t burst like a bubble.

..........................................................

Michael Yardney is CEO of Metropole Property Strategists, which creates wealth for its clients through independent, unbiased property advice and advocacy. He is a best-selling author, one of Australia’s leading experts in wealth creation through property and writes the Property Update blog.

Michael Yardney is CEO of Metropole Property Strategists, which creates wealth for its clients through independent, unbiased property advice and advocacy. He is a best-selling author, one of Australia’s leading experts in wealth creation through property and writes the Property Update blog.

To read more articles by Michael Yardney, click here