For many, starting a family is an important milestone in life – a representation of growth as an adult, of having a hand in shaping the future, of leaving a legacy. Having kids comes with its own set of financial responsibilities, but one area that investors often don’t give proper thought to is the impact it can have on their borrowing power if they wish to buy their own home or investment property.

“One of the biggest impacts of having children is the simultaneous reduction in household income and the increase in other day-to-day expenses. Becoming a parent is a significant life event – it’s physically, emotionally and financially intense,” explain Molly Benjamin and Betsy Westcott from the Ladies Finance Club.

“When starting a family, it’s more important than ever to make sure your income is secure. Expenses such as extraordinary medical bills for a mother or child, the mother needing to stop working earlier than planned, or realising the car or home isn’t big enough to cater to your new family can be a huge blow to your budget and finances if not planned for.

“Remember, you will be at home more, so expect to see an increase in everyday household bills like electricity, water, petrol, phone, medical care and car maintenance. Whacking these payments on to a credit card can lead to a slippery downhill spiral.

“When it comes to kids and your mortgage application, as a general guide, each child you have can reduce your borrowing power by anywhere from $30,000 to $70,000”

”Unfortunately, many Australians do not adequately prepare their household budgets for the pressures of raising children. Benjamin and Westcott note that “a majority of Aussie families are living pay to pay, and whilst this may be OK for weekly expenses, they often panic when the quarterly electricity bill comes in.”

Working a typical day job, it can be difficult to support a comfortable lifestyle for yourself and your household, particularly if you have little ones, or have one on the way. So, many Aussies are turning to property investment as a means of generating passive income and capital growth over the long term, or making it possible to step away from a nine-to-five job eventually.

But it’s important to consider where your borrowing power sits in all of this. Investing in property as a parent is quite different from investing as a single person or a couple – especially on the financial side.

But it’s important to consider where your borrowing power sits in all of this. Investing in property as a parent is quite different from investing as a single person or a couple – especially on the financial side.

According to government research, it costs around $17,000 per year on average to raise two children – a significant blow to any household’s bank account. As a result, many parents can find their borrowing capacity hampered by the simple fact that the expenses related to raising a child eat up much of their finances, which in turn affects how a lender will view their lifestyle expenses.

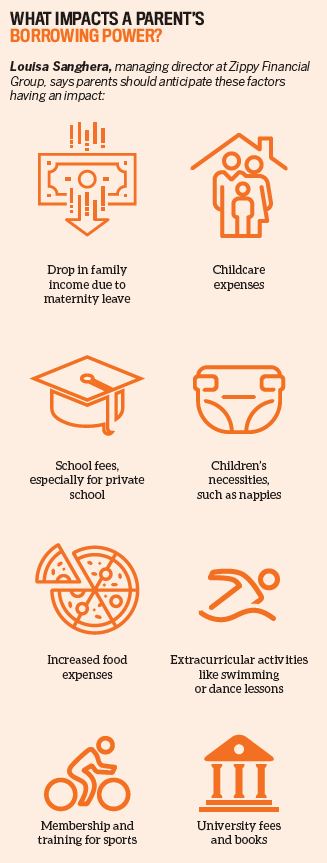

“When you apply for a loan, the lender will assess your living expenses. The exact formula they use will vary from bank to bank, but living expenses are generally assumed to increase with each dependent child you have,” explains Louisa Sanghera, managing director of Zippy Financial Group.

Lenders have been especially careful when it comes to assessing potential borrowers following the royal commission. Sanghera points out that “a $5,000 debt or expense can reduce your borrowing power by around $25,000”.

Getting a loan can therefore be quite trying for those who have heavier household expenditure that includes childcare and tuition.

“When it comes to kids and your mortgage application, there are a range of factors that banks take into consideration, but as a general guide, each child you have can reduce your borrowing power by anywhere from $30,000 to $70,000,” Sanghera says.

“Maternity leave is one of those areas that investors should carefully plan around ... once you drop to a single income, even temporarily, your borrowing power will be impacted”

“Imagine you have three children, each of them going to childcare or private school at a cost of $10,000 each or $30,000 in total per year. This could then reduce your borrowing power by $150,000 – and the bank hasn’t even taken into consideration other costs, like nappies and food.

”Having life insurance, total permanent disability and trauma policies is crucial at this stage, which means additional expenditure.

“If the working parent cannot work through injury or illness and they do not have income protection, the family could end up losing out big time. Most people also do not realise that their insurance provider will not pay for them to take time off to sit by their child’s bedside if they are critically ill,” say Benjamin and Westcott.

Set your priorities straight

Set your priorities straight

The key to being able to balance your finances favourably across supporting children and investing in property is to have a plan.

Benjamin and Westcott advise parents to “review your goals in context of what is your biggest priority – we suggest listing your short- (one to three years), medium- (four to six years) and long-term goals, and then labelling what are needs versus wants. Then prioritise them from most to least important. Starting a family will mean that your priorities change.”

This means that parents need to view monetary inflow and outflow realistically and capitalise on any benefits they may be entitled to.“Get clear on how much the family unit will earn in income. Find out what government support you may be entitled to, like family tax benefits, parental leave pay, dad and partner pay,” suggest Benjamin and Westcott.

“Work out what the family expenses are expected to be, including the upfront costs of having a baby plus the ongoing expenses. Separate fixed expenses, such as the mortgage or rent, insurance, medical, childcare, car, utilities, memberships and transport, from the flexible expenses like food, clothing, entertainment, gifts an d h olidays.

”They also recommend addressing debt as early as you can: “consider what large purchases you might need to make, adjust your spending patterns to ensure your family’s needs are met, pay down debts and potentially get ahead of mortgage repayments so you can take a repayment holiday when the baby arrives”.

You can also save on childcare by getting help wherever you can find it.“

The average cost of childcare before subsidies in Australia is $109 a day but can reach as high as $180 a day in capital cities,” Benjamin and Westcott point out.

Thus, if you can get your own parents, family members or friends on board to aid you, it will go a long way!

Sanghera also notes that parents need to watch out for the little things that cut into their finances almost without them realising it.

“Look for ‘money leaks’ – things like credit card interest, subscriptions and memberships you don’t really use – and any other ways you can reduce your spending and increase your appeal in the eyes of the banks,” she recommends.

“Maternity leave is one of those areas that investors should plan carefully around. If you’re planning to have children, then it might be worth borrowing as much as possible before you go on maternity leave – once you drop to a single income, even temporarily, your borrowing power will be impacted again.”

By preparing to save early, parents can set aside a strong budget for long-term investments.“

One financially savvy couple we spoke to started practising what it would be like to live on their income minus childcare fees six months before the baby was due. That way, when it came to paying for childcare there was no massive shock or surprise, and they had also built up a nice little emergency fund as well,” Benjamin and Westcott point out.

“The best way to build your financial future during this time is to put small amounts often into your mortgage, and salary-sacrifice into your super to make compounding interest work for you. The parents we spoke to who were feeling financially happy and enjoying their time with their new bub were the ones who had planned for and were ready for all financial situations!”